A Financing Fiasco: Making Batteries Bankable

Let’s pick up where I left off in "An Energy Dilemma." ‘All energy is equal, but batteries are more equal than others’ (to really mangle some Orwell). To put it starkly: batteries are better because they make everything else on the grid more valuable.

They make the grid resilient by providing backup power.

They make individual resources, like renewables, more valuable by integrating with them to ensure uninterruptible power supply, thereby turning generation into capacity (we’ll call this batteries’ resource value).

They offer essential grid services by quickly charging and discharging, helping utilities balance electricity without interrupting service, mitigating strain on the grid.

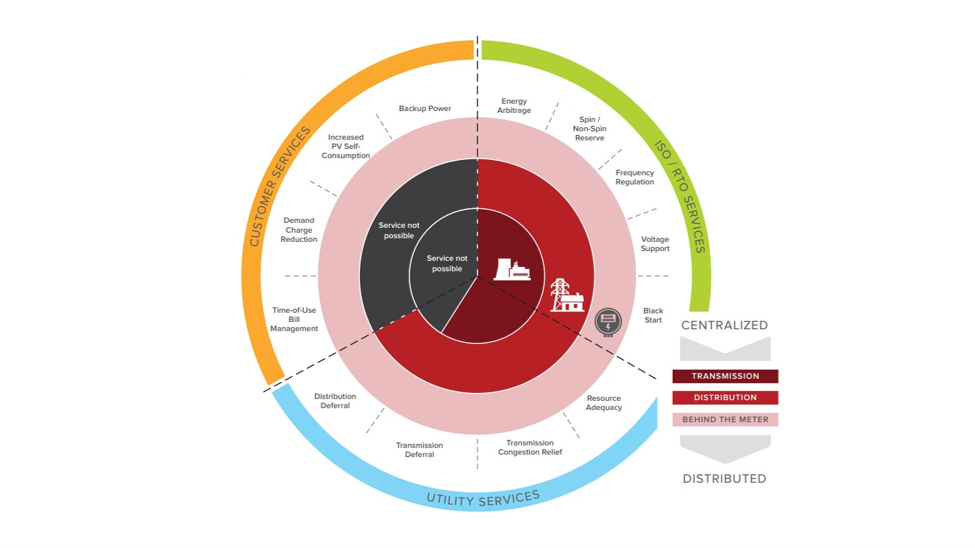

In 2015, the Rocky Mountain Institute put out a report that has been held up as a battery bible of sorts, detailing the unit economics of energy storage. Broadly speaking, it explains that batteries serve three main stakeholders (customers, utilities, wholesale ISOs) and have the potential to provide up to thirteen different services. It highlights that customer-sited, behind-the-meter batteries can offer the most services to the grid but have not been widely adopted due to their unit economics, leaving significant value untapped. Flash forward to 2024, nearly a decade since "the year of the battery" and we’re still seeing that same challenge with home battery adoption. Why?

Driving ROI in Batteries

Battery costs have dropped by ~90% since 2010. That’s enormous, and we’d expect to see a corresponding slide up along the demand curve. Except, even with this price drop, unit economics for home batteries have stubbornly remained prohibitively high for most homeowners. The median battery cost is $1,339 per kWh of stored energy, meaning that a 10 kWh battery (enough to cover a few “critical loads”) is likely to run you over $13,000. For those seeking a whole-home solution or aiming to live off the grid, costs can easily escalate to $80,000-$100,000. Equipment costs typically account for roughly half of the price of a battery system, but battery installation (i.e., labor and project planning) is the largest variable impacting costs. Factors like upgrading electrical systems, installer fees, solar integration, and capacity requirements can bloat these numbers significantly.

Now, just like solar, there are financing mechanisms that homeowners can pursue: cash, loan, or lease.

Cash - Homeowners can pay upfront to own the battery from the start. Although they benefit from quick installation and ownership incentives, system costs remain steep.

Loan - Homeowners can take out a loan to spread the cost over time. Although they benefit from quick installation and ownership incentives, they are beheld to loan terms - which can be difficult in a high interest rate environment like today.

Lease - Homeowners can pursue a lease, renting the battery from a leasing company for a period of time (~10 to 20 years). Although they benefit from quick installation, limited responsibility for upkeep, and lower payments (compared to loans), they may not be eligible for all incentives since ownership resides with the leasing company.

While these financing methods may look the same as rooftop solar, they play out very differently, because of how we value the two resources. Potential investors make decisions based on ROI – i.e., how confident am I that I’m getting my money back, and by when. For solar panels, that’s easy – we can look at generation potential, which flows directly into cash value via self-consumption or selling back into the grid at the going rate.

The ROI for a battery, however, is much more complex, for reasons that start to get obvious when you observe that a battery doesn’t actually generate energy - it can either change when we consume energy (lowering our total energy cost) or dispatch energy back to the grid during peak times when prices are higher (generating revenue). To make batteries bankable, they need to optimize their dispatch potential.

To put this into context, all of the batteries in Texas made 50% of their annual revenue in just 13 days in 2023. Missing one of those days would have put a significant dent in the financial profile of the battery. Unlike with solar, where customers can passively participate in programs, batteries require active management to fully optimize the value of the asset. This provides tremendous opportunity for skilled operators and even more daunting challenges for those who are not. This makes the proposition of financing batteries complex because an underwriter not only needs to underwrite the value of the asset (which is itself a function of a highly volatile energy market), but also the users’ ability to manage it.

Making Batteries Bankable

While making batteries bankable has historically been a challenge, we’re beginning to see a new wave of revenue opportunities for home batteries, sparked by states and utilities looking to get better control of the grid - especially in homes across their jurisdictions. Several states like California are now revising their net metering policies by reducing reimbursement rates (NEM 3.0). This adjustment greatly incentivizes the integration of solar + storage, enabling faster payback (1-2 years sooner) despite higher upfront costs.

With this, we still need to finance the initial cost of home batteries to drive wide-spread adoption given the heightened investment requirements. Fortunately, we are also starting to see states and utilities set up programs to directly incentivize home batteries so that they have more control on the distribution side. Hawaii, one of the first states to scale back net metering policies (2015), has the highest rate of battery attachment for homes in the United States: nearly every PV system installed now includes at least one battery. The driver of this has been their state- and utility-led programs to financially incentivize home batteries through BYOD programs – Bring Your Own Device Programs. And this isn’t just Hawaii. There are now nearly 100 programs across the US that have popped up incentivizing home batteries. These are federal, state, and utility programs that aim to reduce costs for homeowners (tax credits, tax incentives, financing). Even more notably, there are now programs that guarantee financial returns for customers (rebates, performance incentives, VPP programs).

The Bottleneck in Batteries

While these financial guarantees are helpful, they still fail to fill the two core needs of batteries today: 1) the ability to operate with the efficiency of large-scale operators and 2) the ability to finance investments at attractive capital rates.

We’ve seen tremendous innovation in the first of these core deficiencies with companies like David Energy (an Equal portfolio company) and Swell offering automated battery optimization programs that greatly improve the financial performance of batteries. For example, companies like Swell work with local utilities to secure additional incentives on behalf of their customers, enabling new revenue opportunities that wouldn’t be attainable as a stand-alone consumer. Data platforms like Texture (an Equal portfolio company) enable similar optimization capabilities for batteries by partnering with operators, installers, OEMs and utilities to provide more visibility and control of these assets. While still in the early days of this movement, we have confidence that technology can play a meaningful role in helping batteries leverage effective dispatch strategies to capture more revenue, greatly increasing both the consistency and viability of their financing.

However, the second area - financing - has been far more challenging. While we’ve seen some amazing residential-focused battery developers and operators, we’ve failed to see much innovation on the financing of such assets. Most companies are requiring customers to pay out of pocket or are offering financing based on FICO scores. This underwriting fails to incorporate the revenue potential generated by these assets (and how they would impact the income level of the customer). We briefly discussed leasing structures above; however, these are far less prevalent in batteries given the inconsistency in operator performance. Ironically enough, this type of financing exposure is actually heavily desired by large-scale asset managers. We’ve seen Blackstone, Blackrock and Ares all make several significant investments in large-scale storage financing (particularly utility-scale). These financiers are flush with capital from clients seeking energy transition assets as part of their portfolios (or looking to meet ESG requirements), but also benefit from professional operators who are able to effectively leverage dispatch strategies to optimize the value of these batteries (making them more bankable). This in turn reduces the overall financing costs of batteries, further incentivizing deployment of these large-scale assets. Lastly, these asset managers generally feel it’s more worthwhile to underwrite large-scale projects where they can put meaningful money to work, rather than underwriting, monitoring and servicing small-scale projects (this differs from solar, where these players can provide large capital facilities due to the homogeneity of underwriting, performance and servicing).

At Equal, we often look for ways to leverage technology to bring the success of enterprise players downstream to a larger base of buyers. As we look to the success of large-scale deployments, it becomes increasingly clear that the ability to leverage effective dispatch strategies enables lower financing costs. As investors, we’ve put our money where our mouth is, already making investments in companies that are accelerating this space forward. What we need to see next is for capital markets to step up with innovative financial solutions that recognize the improved bankability of residential assets. Most residential battery portfolios still struggle to meet the scale required for large-scale asset managers, but we believe early market entrants will likely garner the greatest returns.

To unlock the bottleneck in batteries, we need to marry technology capabilities and financial capital in a way that makes batteries bankable. While this has been elusive to date, we’re more optimistic than ever that an inflection point for batteries is just ahead.