Competitive Specialization in Founder Support

Rethinking how we serve founders

Follow the discussion on Twitter

As I look at the vast majority of venture partnerships, they’re structured like a fleet of pirates under a single flag. Your objective as a GP is to source deals, win them and then to sit on the boards of those companies. The primary point of connection you have with your fellow partners is around your partner meetings, offsites and fundraising — at many firms, partners were only required to be in the office one day a week (well before the pandemic), spending the vast majority of their time with their portfolio companies or networking with other investors.

For a lot of firms, this makes sense. There are clear economies of scale to the venture business. Services like finance, accounting, legal, fundraising and admin support are all best amortized across a broader base — these services cost a disproportionately higher % of every dollar invested for smaller funds. On top of that, there are natural benefits to creating a larger portfolio to achieve the benefits of diversification (a lot of LPs wouldn’t invest in a solo GP that did one deal a year for a portfolio of five companies). With this, it made sense for GPs to band together as individuals to pursue the mutual shared interests of an investment portfolio as a partnership.

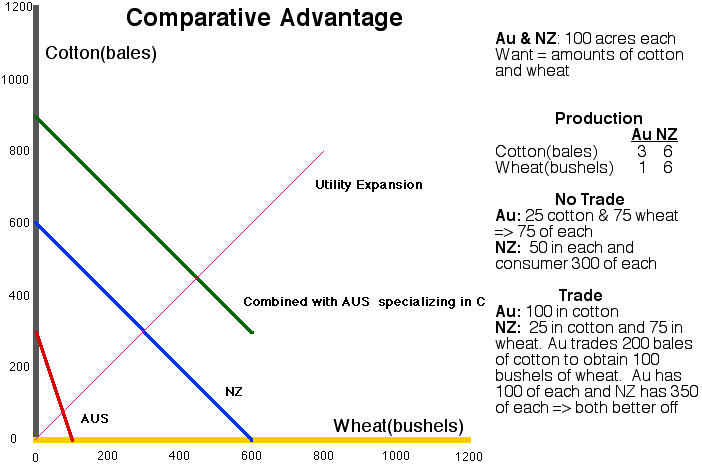

I’ll return to this in a bit, but want to touch upon the concept of competitive specialization. Competitive specialization is a concept in economics where various parties trade with one another based on their localized competitive advantages. For example, parties in the USA (Miley Cyrus reference not intended) may transact with Korea, trading specialty pharmaceuticals (something that the USA has historically demonstrated a leading edge in given our sophisticated research labs and IP protections) in exchange for semiconductors (something Korea is considered a world leader in given their strengths in chip manufacturing). Specialization in the comparative advantage in each localized economy enables each country to dedicate resources to advancing those capabilities, rather than attempting to be the jack of all trades. In a free environment where transaction costs are minimized, specializing in comparative advantages allows each country to hit a higher level of productivity, while driving prices lower to end customers, creating surplus for both sides. (The diagram below demonstrates how competitive specialization between two nations, in this case specializing wheat and cotton production, enables their total combined output to shift higher compared to unspecialized production or self-sufficiency.)

As I think about how venture firms are structured, very few operate with competitive specialization. In private equity, however, this is much more standard procedure. Given the size of the investments and concentration of the portfolio in PE, there are multiple leads on every company, all with different complementary specialties. On any given deal there could be someone whose job is to source the deals, another team member’s job is to analyze its finances and diligence the company, another whose job is to be on the board and others who are going to help the company with various levels of operational or industry expertise. This mirrors what we did in consulting. If we were doing a utility M&A consulting assignment, it wasn’t just the partner who found the opportunity — we brought a team together that had utility, M&A and whatever other forms of complementary expertise we needed to make sure the client was wowed by our service. We all worked the assignment together (contributing where we were best) and share the attribution. Over the last decade, we’ve seen platform strategies evolve that have been able to replicate some of this capability, opening the door for us to think about the best practices of a venture firm in a different way.

Over the last year, I’ve increasingly become aware of the merits of competitive specialization within firms. Last year, we adopted a “Product Owner” strategy where our firm would have dedicated industry leads who were responsible for leading our efforts (sourcing, research, branding, etc.) in those verticals. Product Owners also lead deals and sit on boards, but their role is decidedly different from a generalist like myself. While I’ve long enjoyed the opportunity to do research, develop new theses and get in the weeds of an industry with insiders at the watering hole of a conference, doing this across four domains is tough. Through this transition, our Product Owners have taken the reins on those activities, enabling me to pull back on those activities and focus more heavily on sourcing deals, selling our firm to founders, incubating companies and working with my founders. These are the areas that I enjoy the most and are the areas in which I believe I have comparative advantage. You’ll even notice that I haven’t written an industry-focused blog post in months. I now get to focus my time on concepts like this (that I find really stimulating), while our team leans in on a lot of the industry activity.

This isn’t just about the division of labor, it’s about empowering our team to be the best (and happiest) versions of ourselves, while putting multiple heads on every company to deliver an unparalleled offering to our founders. We recently competed to lead a deal for a startup led by objectively some of the most impressive backgrounds I’ve ever seen. The founders were ideating a concept in a market that I knew well, but as we dug deeper into the nuance, it was the expertise of our Product Owner who could achieve a level of depth that I frankly couldn’t (and I think most of you know, I get pretty frickin’ deep! 😊). Their depth enabled me to focus on some of the areas where I could be more helpful (primarily, thinking through strategic frameworks for the business model and connecting the founders with industry leaders in my network), while giving our Product Owner an opportunity to shine (and they did!). I don’t think we would have won that deal (and we did!) if it were just me. Ultimately, it wasn’t just the division of labor, but rather our specialization of skill sets that enabled us to bring a package that was truly unique to the founders and I’m increasingly realizing how different that is from anything I’ve traditionally seen in venture.

So many venture firms focus on progression looking analogous generation-to-generation. Emerging partners are mentored by the ones before them and mimic their style, investment philosophies and operating principles. Again, this CAN work, but perhaps there is another way that can be equally or even MORE successful. Our Product Owners will not follow my same flight path, but they are ultimately stealing more and more of the time and attention of the founders and industry partners we work with. While it was scary at first, our Product Owners stealing the ball from my hands has been a welcome revelation, enabling me to increasingly focus on finding my own areas of competitive specialization (with the dual benefits of seeing them progressing, while doing something they love) and frankly, the type of work I enjoy the most.