Ephemeral Margins in AI-Native Services

Follow the discussion on X here

As folks evaluate AI-native services, I see tremendous belief (faith?) that initial product pull and lower cost will lead to long term structural value. Unfortunately, this isn’t always the case.

You can look through the ticker tape of time to see ample evidence of technology innovation yielding lower costs to customers, thus enabling early adopters of those technologies to seize market share. This is the foundation of the American industrial economy. Many players competing to out-innovate each other to produce bigger AND cheaper in the interest of economies of scale.

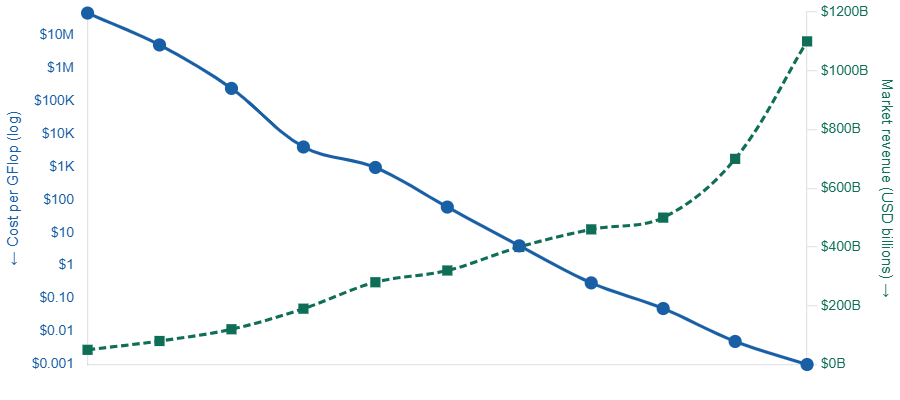

In some cases, this can be highly successful thanks to the concept of Jevons Paradox. We’ve explored this phenomenon before and it explains how, as the cost of a good/service comes down on a per unit basis, it opens up the scope of serviceable customers, thus driving higher overall consumption (expanding both the TAM and the profit pool for the market). We’ve observed this trend for decades in the personal computing market. As the cost of computers (relative to their performance) follows Moore’s law, we subsequently find new uses for consumption. As you can see below, while the price per unit of compute has fallen >99.99%, the overall TAM has grown dramatically as the growth in demand has more than offset those price declines. This is the story playing out in AI right now - demand growing as the price per unit of a computing function comes down.

But what if demand is fixed? AI is being applied to endless labor markets where demand is indeed fixed and the same supply side phenomenon (i.e. declining price curves) remains in effect. To give context, think about the market for auto insurance claims processing in a given year. When a car accident happens, there are two costs: 1) the cost of the actual claim (to fix or replace the car), and 2) the cost to administer this claim. The process to administer that claim is laborious and represents a great use case for AI and automation. With that, we’re seeing a LOT of companies attacking this space and many are demonstrating lots of traction by offering an AI-enabled service at a dramatically cheaper price than legacy players. Many of the emergent players are happy to offer their service below cost with the belief that 1) winning the market is all that matters, and 2) with scale, their margins will improve. In many markets, this can make a lot of sense, but not in commodity markets with declining pricing curves and fixed demand.

Instead, these folks are inciting a race to the bottom…one where margins disappear. As I spoke with one leading insurance industry exec, they said “We use 34 different TPAs…they are all getting cheaper as we bid them against each other…it’s beautiful.” These players are collapsing prices (and margin) in the market with no clear route to winning the market (TPAs typically have very low switching costs and the quote above shows how prevalent multi-homing is). When prices decline and demand is fixed/inelastic (i.e., demand doesn’t increase with lower costs), the market significantly decreases (see below) as does the margin structure for the industry. Even worse yet, these companies end up on an endless hamster wheel for customers. When prices decline by 50% in a given year for an industry structure like this, companies need to double their customer count just to maintain themselves.

As we see these companies, the margins are ephemeral. They initially swell as the insurgent player finds a way to innovate cost structure and grab market share, but then disappear as other new entrants come in and drive prices down. Making money in these markets is like being stuck in quicksand…the harder you compete cost structures down, the closer you bring yourself to your own demise.

We’re deep believers in AI-native services at Equal Ventures, but understanding how industry cost structures will evolve can make or break your company. There are nearly limitless markets that have and will expand dramatically with AI and if you’re a founder in our core sectors looking to win those markets, we’d love to hear from you.