F*ck Abundance

Join the conversation on X or Linkedin

With a barrel of oil hitting over $100 per barrel, energy prices have come into mainstream focus a lot lately.

For those of us in the energy sector, however, energy prices have become a dominant focus of the last year as the demand from hyper scalers contributes to escalating prices. This trend, however, isn’t solely the fault of hyper-scalers or even the latest conflict in the Middle East. A few years ago, the climate narrative shifted from “sustainability” to “abundance” - a belief centered around the ability to produce endless clean energy, to justify its own consumption. As a life long climate professional, I’m here to say “Fuck Abundance”.

Our economy is already at a fickle state given inflationary concerns and the persistent mindset around unlimited energy consumption places systemic risk to the livelihood of everyday Americans. Utility bills used to be a nuisance…now there can be months where your utility bill is more than your mortgage. Reducing energy consumption used to be a sustainability imperative, but it’s now become an absolutely necessary economic imperative as you’ll see in the data below.

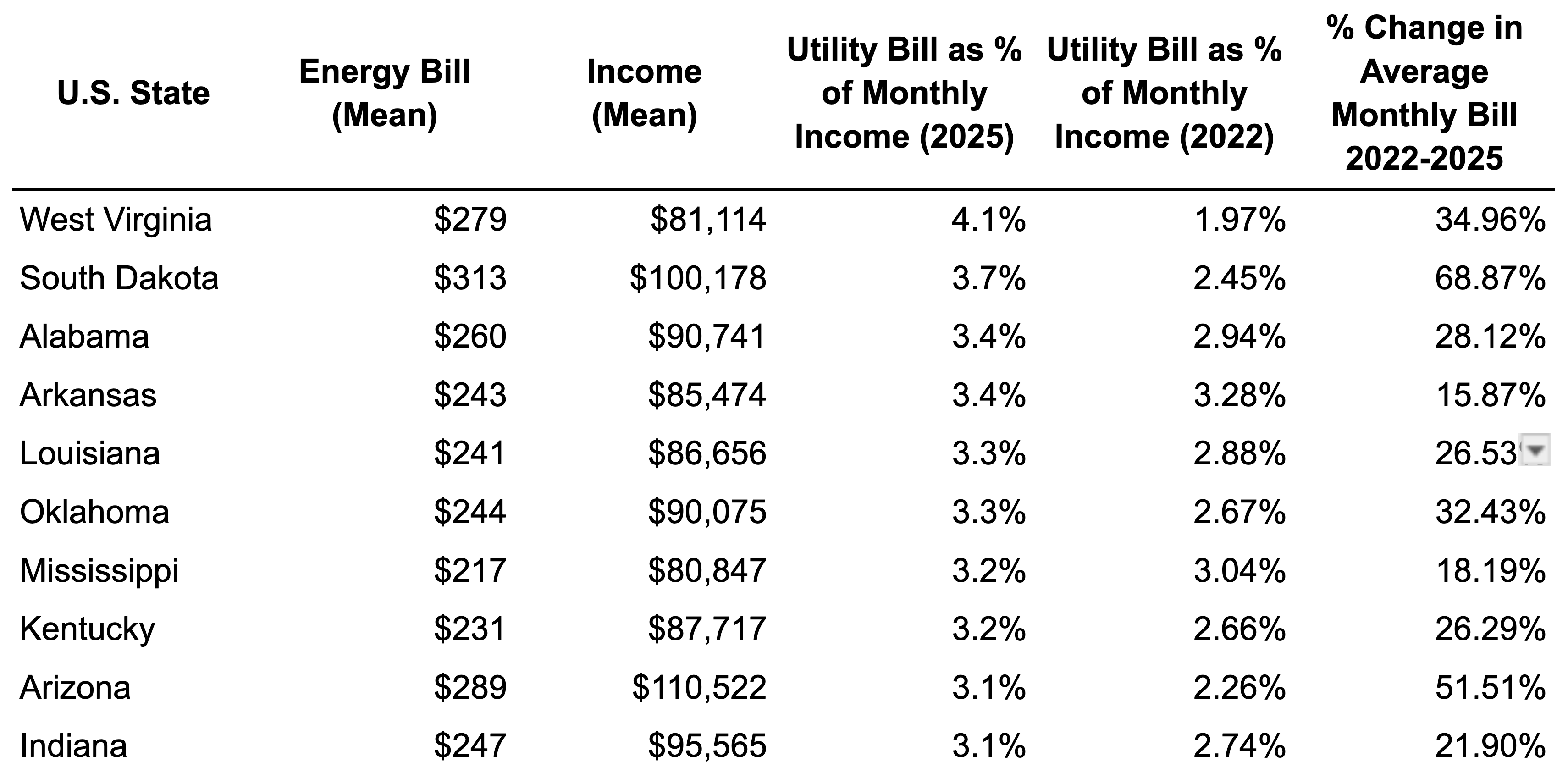

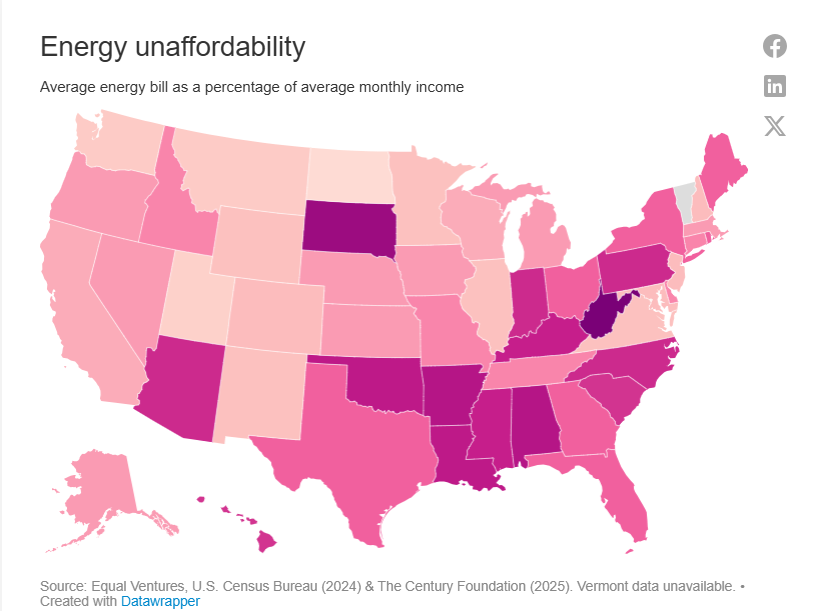

These 10 states are the ones paying the highest % of their monthly income to utilities and the rise in that % has been fairly dramatic over the last 3 years. Keep in mind, the incomes listed here are based on the average income for the state. Those in the bottom third of median incomes spend 16% of their income on energy. And, the utility bills listed here are the average over the course of the year, which is subject to volatility that could make a given month significantly higher than others. When you combine this with the fact that most lower income homes tend to be less efficient than higher income homes, it’s easy to see how utility bills could become a significant impediment to the individuals living in these states.

Equally interesting is the political composition of these states. Every single one of these states went “Trump” in the 2024 election. Counter to the narrative, these aren’t states that are experiencing inflated prices due to investments in clean energy and sustainability, they are actually the ones experiencing the greatest challenges because they didn’t (albeit South Dakota leverages a heavy dose of wind power). The result is that the average American in these states is being hurt.

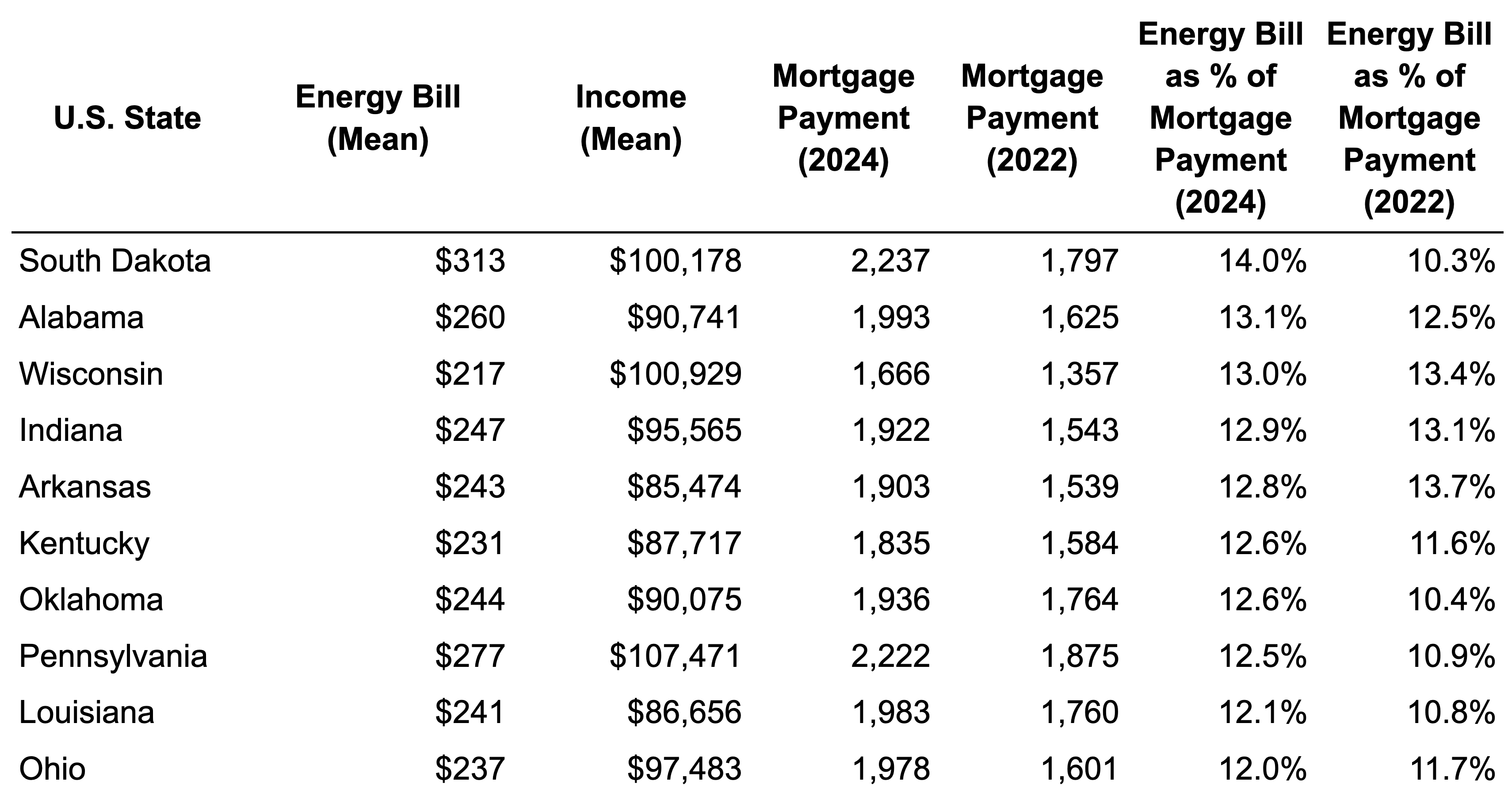

Another lens that we thought worth looking into were utility bills as a % of a household’s mortgage payment (see below). Folks in South Dakota are now seeing their utility bill be 14% of their mortgage payments. In many cases, that’s going to be significantly more than their property taxes or other monthly household expenses. Anecdotally, I spoke with a homeowner in Pennsylvania who said that their utility bill in January (which was historically cold) was higher than the mortgage payment they had on their home. The average American isn’t used to paying 2 mortgages at once, so this has the potential to place meaningful household harm. Perhaps even more alarming, utility bills represent an even higher percentage of median rent.

The list above remains largely republican leaning, but the introduction of a few “purple” swing states is intriguing. This affordability crisis is largely removed from the surge in data centers. While Ohio and Pennsylvania are growing hubs, most of the other states on this list have relatively benign development. The states with the most data centers per capita including Virginia, Texas and California, would rank 19th, 27th and 48th for “Energy Bill as a % of Mortgage Payment (2024)”. These states are seeing booming AI / data center demand, while investing heavily in clean energy and sustainability, and are subsequently seeing dramatically lower bills as % of the relative income and housing costs.

The fact of the matter is that this problem is going to get a lot worse before it gets better. Our power generation infrastructure is decaying at an alarming rate as coal, nuclear and hydro facilities are extended beyond their previously believed useful life. As hyper-scaler demand continues to grow, supply can not come on fast enough to meet their demand. My contacts within large organizations that are seeking to bring more energy capacity online are sharing that they can’t even get turbines for at least 2.5 years (even when cutting to the front of the line), meanwhile the permitting backlog of projects results in an average lead time of ~4.5 years and the only 19% of projects requesting interconnection from 2000-2019 made it to completion by 2024.

Rising energy prices are ultimately a function of supply and demand. For better or worse, the ability to dramatically impact supply in the short-term is hampered by technological and regulatory impediments. While we can invest in these and progressively address over time, there is only so much we can do to address near-term supply. Given the extent of energy price escalations, why would we confine ourselves to a single side of a two-sided market? Giving up on demand-side management in cutting off half the addressable opportunity.

This is part of the reason why we find batteries and the concept of Virtual Power Plants (VPPs) so compelling, but they are unlikely to be enough and come with their own permitting and supply chain constraints (along with other environmental and economic externalities). The reality is the business case for investments in energy efficiency has dramatically improved amidst a time where we are not only seeing dramatic rises in energy prices, but also dramatic technology advancements that can cut into the largest cost center of energy efficiency - the soft costs of designing, evaluating, delivering and monitoring these projects. Truth be told, many of the largest energy efficiency opportunities are centered around automation and optimization of existing infrastructure, which requires little or no capital investment. We don’t need to build a new grid right beside our partially utilized existing grid, funding tons of new hardware / capex. Instead, we can and should make the grid we have run MUCH more efficiently. Nonetheless, the concept of energy efficiency tends to fall on deaf ears as we continue to pursue our obsession with consumption under the premise of “abundance”.

Unfortunately, we’ve seen this show before. For decades, the oil industry lobbied to expand recycling as means to promote continued demand in plastic production. Beginning in the 1970s and accelerating in the 1980s–1990s, major oil companies and chemical producers—including firms like ExxonMobil, Dow, and Chevron—funded trade groups and public campaigns to convince Americans they could “have their cake and eat it too”. In this fantasy, there wouldn’t be environmental consequences to the unlimited use of plastics, since the plastics would be recycled. Yet here we are 50 years later and only 9% of plastic is actually recycled and we have a pile of plastic sitting in the Pacific Ocean that is twice the size of Texas.

The reality is that you can’t have your cake and eat it too. We need to find ways to curb consumption (especially peak energy demand) to avoid catastrophic outcomes - both economically and environmentally. “Sustainability” no longer motivates this large-scale behavior change, but kitchen table MATH can. The ROI of investments in grid utilization and energy efficiency make sense and are overdue. We need to put storytelling of a make-believe energy economy aside to focus on the math. Failure to do so does nothing more than to hurt the average American.

“F*ck Abundance”

the states that skipped clean energy investment are now paying the highest energy bills as a percentage of income. very interesting to read about the abundance narrative!