Hidden AI – How to “eat” your AI to monopolize markets

Follow the conversation on LinkedIn

Core to Equal’s investment philosophy is finding ways for technology to have impact where it’s previously been under-utilized. While there are many markets where there are known buyers for high functioning products, we’ve witnessed many large markets that experience extremely limited willingness-to-pay for software where it makes more sense for startups to “eat” the core advantages of their IP. My colleague Ali highlighted this in one of our most recent posts, introducing the concept of “Hidden AI”. For these companies, AI is at the core of their competitive advantage, but is rarely seen to the end customer. On the outside, they appear to operate much like incumbents, but underneath the surface is where all the competitive advantage lies.

Certain industry segments will have more or less price elasticity to tech adoption, but just picking the right industry for this type of model isn’t enough. Determining “how” to eat your AI is equally important. To illustrate this, lets look at the insurance industry with a few of our portfolio companies.

Two of our portfolio companies, Stand Insurance, a next-gen property insurance company attacking climatic risk, and Equal Parts, an insurance agency aggregation platform, are two core examples of “Hidden AI” at work. These companies operate seamlessly with customers and stakeholders in the legacy value chain. Outsiders rarely know they are interacting with anything that is AI-related when they work with us – they just know they are getting incredible products/services at incredible prices. On the back end, however, AI is at the core of both of these businesses, enabling Stand to underwrite and mitigate risk in ways that were previously unimaginable and for Equal Parts to see 60-70% reductions in OpEx over legacy agencies.

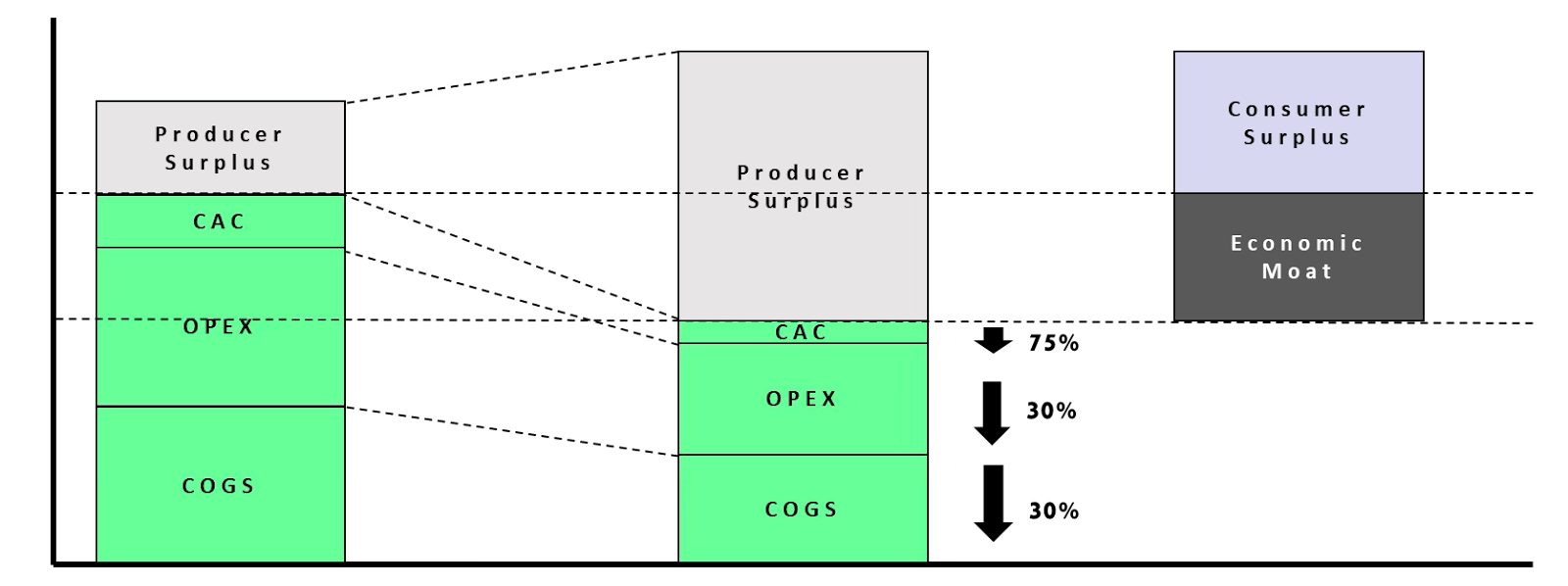

If you look at the industry cost structures for these segments (carriers and brokers), the most significant cost segment for carriers is COGS (the losses they accumulate for the policies they underwrite) and for brokers, its OpEx (the wages for various staff to service business). While much of wave 1 insurtech companies focused on decreasing CAC and increasing WTP (which largely proved fruitless), those economic parameters are important, but simply don’t provide enough leverage to win the category. Being 50% better on CAC (which might represent 10-20% of the total policy value), doesn’t matter if you are running a loss ratio of 105% of policy value (which many wave 1 insurtechs were) compared to others in the industry operating at 40-60%.

We often use the graphic below as a way to identify which cost structures are most applicable for a given company in its industry segment and to determine what would be necessary to develop, sustain and compound a unit economics advantage (or what we refer to as a “moat”).

For both Stand and Equal Parts, their core IP is focused on the most expensive parts of their industry cost structure. Winning on those cost structures (and having a significant edge on those cost structures) provides the potential for a monopolistic position in those markets. Needless to say, this has enabled these companies to grow phenomenally quickly with outstanding economics. Having worked closely with insurance carriers and brokers for the last decade, I have no doubt that these companies internalizing their AI is the far superior to selling it.

This isn’t to say you can’t build great companies attacking other segments of the cost structure. Another one of our companies, Isomer, is an agentic platform for transforming the operations of insurance carriers. This is a cost segment worth hundreds of billions of dollars, but its hard to be a carrier that can when on OpEx excellence alone. In their case, its far better to sell their services to as many carriers as possible. Given the size of their market and the benefit to their end customers, this is still a tremendously large market opportunity. Both these approaches can yield category defining $10b+ companies, but knowing when to implement each is highly dependent on the cost structure and competitive dynamics of your industry segment, so make sure to do your homework in advance.

Hey Rick, thanks for sharing this. I just graduated and have been working on an AI code documentation tool. Given you obviously know what you're talking about, would you be willing to talk or answer a few more specific questions? hjconstas@docforge.net