LESSONS FOR (AND FROM) A CRISIS

By: Rick Zullo, Co-Founder & GP @ Equal Ventures

By: Rick Zullo, Co-Founder & GP @ Equal Ventures

We are in unprecedented times with the markets experiencing some of their deepest declines on record and, more importantly, the world is experiencing the most severe pandemic crisis it has seen in the last century. I am not qualified to judge the extent, severity or duration of this crisis, but as someone on the front lines of the two previous market failures (the “Cleantech Bubble” and the “Credit Crisis”) and a perpetual student of markets, I wanted to share some of my lessons learned from prior crises to help others who haven’t experienced times like these before. Our hope is that these learnings help you and your company navigate the crisis ahead.

Be Aware of the Appetite for Risk

We’ve experienced a more-than-decade-long bull-run that has led to what some may call irrational expectations for the valuations of public and private companies. Even after the market’s significant contraction, we are still seeing market multiples in-line with historic levels, whereas one might expect those multiples to fall below given liquidity constraints, capital preservation, market psychology or systemic impacts this crisis may have for future performance. For nearly 11 straight years, there was “easy money.” Unfortunately, “easy money” doesn’t exist. As Charlie Munger, famed investor of Berkshire Hathaway, once said ‘[Investing is] not supposed to be easy. Anyone who finds it easy is stupid”.

Easy money is laden with risk and this crisis has served as the catalyst for a pendulum swing away from risk. For the last decade, there has been limited thought toward risk management in both the public and private markets. We’ve seen:

Consumers lever themselves to levels that are worse than prior to the credit crisis

Retail investors aggressively expanded both their overall appetite and that for exotic / non-traditional products (alternative investments, options, crypto, etc.), while savings rates have dwindled to incredibly low levels

A surge in the “gig economy” that is leaving many workers without pay now that the market has contracted and offline work is put to a halt

I’ve long felt that a recession was inevitable (as many others have) and that these factors would ultimately amplify that recession. These factors are coming to bear in severe ways that likely impact the consumer and the national economy far more than most tech companies who benefit from recurring revenue and seem better positioned for “work from home”. That said, through my conversations with other investors over the last week, it’s clear that the tech market will be significantly impacted as well.

Appetite for risk has led to valuations achieving levels that many companies will have severe difficulty living up to in this new environment. The market’s momentum led to a tremendous amount of paper gains which may experience significant discounts given multiple compression and the lack of liquidity. Many VC firms will ultimately have to pick winners and losers across their portfolio (as they did in 2000 and 2008) and it’s likely they will focus their dollars and time across their biggest positions at what will ultimately be lower valuations and unfortunately seeing higher loss rates across their portfolios.

It’s impossible to predict a “Black Swan” event, but the very task of risk management mitigates its impact during times like this. Unfortunately, very few have been thinking about risk management from the venture side, choosing to raise bigger and bigger funds, keep companies private for longer and longer, and chase momentum oriented deals for the “easy money”. These funds have unquestionably outperformed over the last 10 years, however, they are those likely experiencing the most pain right now. As Warren Buffet once said, “Only when the tide goes out do you discover who’s been swimming naked”. Unfortunately, many in our industry have been skinny dipping for a long time and this crisis is pulling the tide out even further than anyone could have expected. This is exactly what happened during the Credit Crisis as the appetite of Wall Street became far too veracious without concern for risk, leading to a >50% fall in the Dow in less than 6 months (keep in mind we are only down ~30% as of this writing).

How Quickly Value Can Disappear When Relying on a False Set of Assumptions

Early in my career, I worked extensively in cleantech and found tremendous promise in many of the emerging technology companies in the space. Investors flooded the market with dollars, often in companies with radically different operating profiles than what they had ever invested in before (i.e., CAPEX intensive manufacturing into commodity energy markets) and much of this under the assumption that an eventual price of carbon via legislation, would make many of these technologies economically viable. Unfortunately that never happened. I remember distinctly when Harry Reid announced that the Senate would abandon its pursuit of Carbon Cap-and-Trade legislation in favor for pursuing healthcare as their legislative priority. I was in the midst of interviewing at various cleantech oriented VC firms and those conversations evaporated almost overnight. Venture firms were no longer hiring, companies that looked viable no longer were and the sector became an instant pariah.

I say this to highlight how quickly value can disappear when the case for a company’s (or market’s) value is based on a narrow set of assumptions. This was just as evident through the Credit Crisis as it was during the Cleantech Bubble, where assumptions on diversification and ever rising real estate prices ultimately crippled our financial system. Dependency on a few factors is not what risk management is supposed to be. I suspect the current valuation of many growth stage companies is dependent on a narrow set of growth factors that will be extremely difficult to achieve in this new normal. If you are a CEO and haven’t stress tested your business under recession scenarios prior to the crisis, stop reading this and do it immediately. If you are an investor, determine the assumptions your companies rely on and assess their viability if those assumptions are no longer valid in the current environment.

The second note to take from the Cleantech Bubble is regarding investing in your “wheelhouse”. Many have written about some of the mistakes VCs made during the Cleantech Bubble, some of which include investing in categories where they ultimately didn’t understand the underlying technology. For years, I’ve held perhaps an overcautious weighting to “investing in what I know”, choosing to opt for depth over breadth. This is a direct response to those cleantech days where I saw founders and funders fail to find common ground when times were tough. This is more important than ever now. Both VCs and founders require insight into the sectors they are participating in to navigate tough times like this. VCs will ultimately allocate their capital to the companies they have the most conviction in and ultimately sector expertise is one of the key determinants of that. Founders, similarly, should preserve their capital for the products and projects that they have the most confidence in and surround themselves with investors that understand their markets best.

Knowing When to Practice Patience and Opportunism

In crises, cash is king. For public market investors, 2009 was the reward for years of patience and conservatism prior to the crisis. If you invested in the NYSE in January of 2009, you saw a >3x return over the next 11 years. 2009 was the year that value investors dream about and gives justification to the trademark patience that most value investors demonstrate. Charlie Munger once said “The big money is not in the buying and selling … but in the waiting” and 2009 proved to be the point waiting for, enabling them to buy assets at unprecedented value and benefitting from the coming decade of growth.

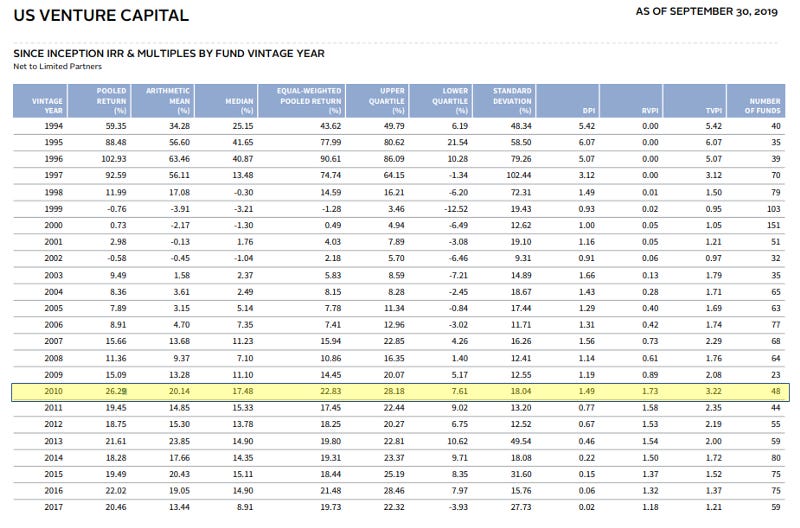

Similarly, the 2010 seed stage vintage (the first vintage coming out of the crisis) included a broad swath of high performing funds. It was and remains, the best performing vintage since the dotcom bust (see below). That said, it’s unclear that the bargain hunting tendencies of the value investing world translate to that of venture where our industry has such a propensity for “winner take all” dynamics. Capital flight toward “best of breed” applies to both VC funds (as we interface with our LPs) and to founders (as they interface with VCs). Public companies are generally cash flow positive, startups generally aren’t. Timing and the length of this crisis will unquestionably change the calculus of survivability for companies across the board and “bargains” may ultimately have difficulty raising downstream capital if conditions persist..

Great companies are indeed born out of times that are good and bad, however, the winning dynamics of the 2010 vintage may have less to do with “bargain hunting” and more to do with the concentration of capital and resources into the “best of breed” in the midst of reduced competition across managers. In 2009, VC funding fell to $22b, down from >$31b in 2007. Competition fell significantly and the market was ripe for what would be a historic recovery. For context, VC funding in 2019 was >$107b, nearly 5x higher than 2009 levels, leading to downstream capital for years to come and historic valuations as those companies hit maturity. I’m not sure we’ll see the same type of fall in the venture markets (if so, many GPs will be out of business), but consolidation amongst the GP community would likely lead to better returns for near-term vintages.

I’ll leave it to GPs and founders themselves to determine if now is the time to be patient or aggressive, but would caution against catching the “falling knife” and note that investing in public markets in 2010–2012 (after the bottom was fully supported) yielded much of the long-term return as investing at investing at the market low in 2009. The value of the NYSE in November of 2012 (nearly 4 years after the market bottom in March of 2009), was at the same level as September 2008, less than 6 MONTHS before the crisis. Similarly for venture, every single vintage since the Credit Crisis has outperformed those in the 10 years prior to the crisis. Timing a bottom is incredibly difficult and moving too early can be extremely hazardous, with often the best risk/reward dynamic existing in the early days after the recovery when support levels have been established.

Whether you are a founder, GP, LP or even a public market investor, one thing is certain, cash is scarce right now and those who have it, have an advantage. If you’re in that fortunate camp, choose wisely when/where you want to deploy it, balancing patience and opportunism.

This Time is Different, It Always Is

At one point last year, I asked one of my mentors whether this market bull-run felt different than those that he had seen in the past. He said, “Yes, but it always does”.

While I hope this advice is helpful, I want to caution that this crisis seems far different than those that I have experienced in the past. For both the Credit Crisis and the Cleantech Bubble, these were crises that were somewhat isolated to their sectors and represented an erosion in asset values and economic conditions, not a threat of widespread loss of life. Economics and asset valuations are things that most founders and investors have some understanding of, pandemic viruses are not. It’s impossible for me to gauge the extent, severity or duration of this crisis, but it feels notably different in terms of the disruption to daily life and its economic reach (which have the potential to be far more diverse and widespread if the pandemic persists). Above all else, this crisis is associated with a significant loss of life, which certainly distinguishes it from any other economic crisis that I’ve seen since September 11th.

In times like these, knowing what you don’t know is often more important than knowing what you do. Information quality is improving daily, likely enabling a greater understanding of how this crisis will impact the broader market, our industry and your company. Just remember, founders and VCs alike are judged not on a quarter’s worth of results, but those over a 10 year time horizon. Taking that mindset into every decision you make right now is critical as a single miscalculation could make or break your business in a world of so many unknowns.

The market WILL recover, liquidity WILL improve and the virus WILL abate. My hope is that knowing 1) where we are on the risk spectrum, 2) how quickly value can disappear when valuations are predicated on a false / narrow set of assumptions and how to stress test those assumptions and, lastly 3) when to practice patience and opportunism, will help us navigate this crisis. These are a few of my lessons from prior crises that I’ll continue to use to navigate today’s events and wish everyone the best in the days/weeks/months/years to come.

Stay safe.