Social Commerce Liftoff

Shopping increasingly shows up disguised as entertainment. The purchase feels less like a transaction and more like a natural conclusion to a story that your brain has already rationalized.

Impulse buying is not new. What’s new is how efficiently social commerce manufactures the moment. Entertainment contexts, creator-led trust, and algorithmic feeds now do the merchandising for you, shaping why consumers want to buy in the first place. This shift is forcing brands to rethink demand formation as something that happens upstream of the storefront, in places they do not fully control, on timelines that do not respect traditional planning cycles.

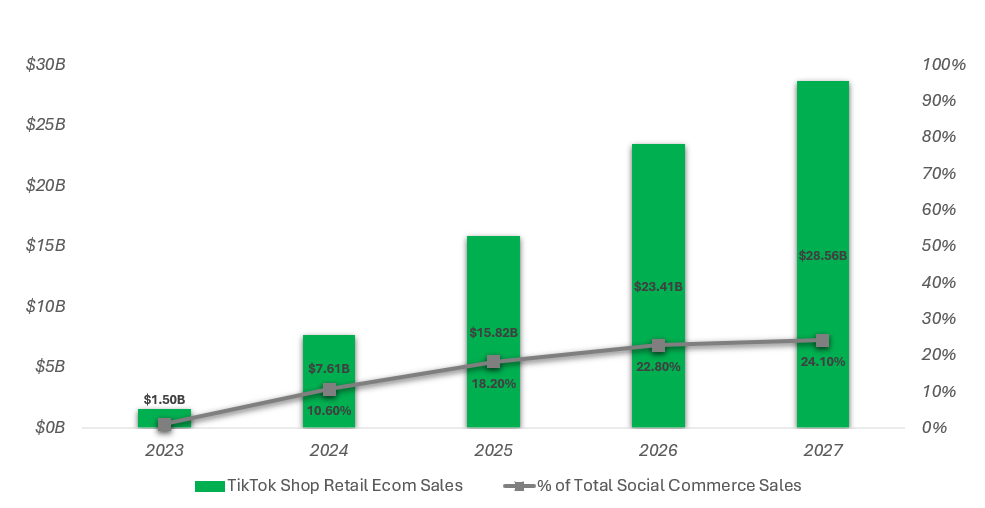

The scale of this shift is already meaningful. US social commerce sales reached $87.0B in 2025 (up 21.5% YoY) and the category is projected to surpass $100B in 2026. TikTok Shop alone hit ~$15.82B in US sales in 2025 and is projected to exceed $20B in 2026 and $30B in 2028.

TikTok Shop Retail Ecommerce Sales

Source: EMARKETER Forecast, November 2025

Importantly, the above growth does not currently represent category sales dominance. Social commerce only represented 6.9% of US retail ecommerce sales in 2025, and ecommerce itself was projected to be ~16-17% of total US retail sales in 2025, with Q3 2025 data totaling 16.4%. These facts can coexist.

Even as a minority share of total retail sales, social commerce can matter disproportionately because it is increasingly the point of origin for consumer desire, reshaping how people buy through entertainment and parasocial connection.

What makes this moment distinct is that every major platform is now reorganizing around social commerce simultaneously. YouTube announced in-app checkout for 2026, with over 500,000 creators already enrolled in YouTube Shopping. YouTube CEO Neal Mohan’s 2026 letter explicitly positioned YouTube as a “premier shopping destination,” adding more optimal brand partnership tools and shoppable links to Shorts, as well as making it easier for influencer marketing agencies and brands to find and hire creators.

Instagram is increasingly a discovery engine built around short-form video. Reels captured 46% of total time spent on the platform in the US, up from 37% in 2024, while more than half of Instagram ads now run in Reels. Whatnot recently raised $225M at an $11.5B valuation, generating $6B in GMV in 2025, more than 2x in 2024 with high engagement, about 80 minutes per day and 80% month over month retention.

This is not limited to a single product vertical. “For TikTok, health, wellness, and beauty are top categories, followed by accessories, household items, fashion, and cosmetics,” according to EMARKETER. They go on to state that TikTok Shop’s best-selling items combine low price points, spur-of-the-moment appeal, trendiness, and they rely heavily on strong creator amplification.The breadth of categories gaining traction signals that creator-mediated commerce is becoming a general-purpose distribution model.

We see a number of opportunities as the market moves from renting attention to building scalable entertainment distribution.

Owning The Narrative

Both performance marketing and creator-led commerce are probabilistic systems. The difference lies in who owns the persuasion. In performance marketing, the brand controls the message and pays to put that message in front of people. In creator-led commerce, the brand delegates persuasion to a trusted curator and pays for access to that curator’s credibility, audience, and conversion ability. That works! But brands know that renting credibility comes with structural tradeoffs: you don’t fully control the message, you don’t fully own the audience, and you do not always retain the learnings in a way that compounds.

So, brands are starting to internalize the function, copy-cating mega-creators for insight. MrBeast’s listing for a Creative, Viral Marketing role is exceptionally explicit about the new composite skill that brands are scrambling to hire: someone who can “build engines, not campaigns” and “convert cultural moments into sign-ups, activation, revenue, retention, and repeat engagement.” That is a very different mandate from traditional brand marketing. It is much closer to a creator-growth operator sitting at the intersection of entertainment, distribution, and conversion.

The same logic is showing up in how brands talk about creators. Kat Chan, senior director of brand marketing at Duolingo, put it well: influencers will become “more core to brands than one-off transactional content.” EMARKETER also quotes Business Insider’s Tameka Bazile making the companion point: rather than simply paying creators transactionally, more brands are pulling creator talent closer to the team itself so they can internalize community, fluency, and virality.

The In-House Creator Stack

Large companies are now organizing around this at the executive level. Gap created its first-ever Chief Entertainment Officer role in January 2026 to build and scale its entertainment, content, and licensing platform across music, television, film, sports, gaming, and cultural collaborations. Gap has labeled that broader strategy “Fashiontainment,” and Richard Dickson later summarized the thesis even more plainly: “Fashion is entertainment, and today’s customers aren’t just buying apparel, they’re buying into brands that tell compelling stories and drive cultural conversations.”

You can see this shift take shape through the commerce infrastructure itself, not just organizational design. Sephora launched My Sephora Storefront in September 2025, an affiliate platform that keeps checkout entirely within Sephora’s ecosystem, built in partnership with motom. Within weeks, the program reached 1,000 live creator storefronts, exceeding internal projections. Condé Nast announced Vette, a creator-led commerce platform launching in early 2026, which lets influencers and editors operate independent curated storefronts with Condé Nast handling checkout and brands fulfilling orders via drop-ship.

Brands are proving that they want to own these channels. Owning the channel means owning the creative, learnings, and ideally the customer relationship that compounds over time. Affiliates and UGC then become variable distribution on top of owned content. Though they must tread lightly as EMARKETER found that 26% of consumers distrust any form of influencer marketing, so ensuring these truly feel like entertainment above traditional advertisements will be a thin tightrope to walk.

The New Operational Playbook

Once you bring the creator function in-house, the question shifts from “did we buy the right traffic?” to a harder set of problems: can we manufacture repeatable hits without turning the brand into a roulette wheel? When performance is driven by a fat-tailed content portfolio (most posts do nothing, a few do everything), the temptation is to chase the last spike. And when brand and creator-mediated content lives across TikTok, Instagram, YouTube, and owned channels simultaneously, this challenge can become genuinely complex.

Furthermore, striking success with virality is an operational stress test. When creator-led commerce works, it produces demand curves that look nothing like traditional retail: unpredictable spikes, overnight sellouts, and second-order effects that cascade through fulfillment, customer service, and inventory planning.

Modern Retail’s Feb 2026 case study on Cakes Body and Béis reads like a field guide to burst readiness: Cakes once hired TaskRabbit to ship after selling out overnight, later filled about 15 customer service roles in 24 hours, and kept the engine running by posting with high frequency and amplifying the best content into paid. Béis adds the second-order lesson: “it’s rarely just that one item.” Stockouts become the start of the next moment via pre-orders, wait lists, and hype-building around restocks.

Even TikTok is learning this in public. ADWEEK reported TikTok reversed a plan to phase out seller-fulfilled shipping in the US after pushback from merchants who argued that centralized fulfillment would reduce flexibility, pressure margins, and make viral demand harder to manage.

The Opportunities Ahead

In a world where commerce channels behave like content channels, with demand driven by algorithmic spikes rather than seasonal planning, brands need entirely new categories of tools and solutions. Demand forecasting that incorporates real-time social signals. Fulfillment infrastructure that can elastically scale within hours, not weeks. Customer service automation that handles 10x volume surges without degrading experience. Inventory systems that can convert a stockout into a waitlist into a restocking moment. The operational stack for creator-driven commerce is largely greenfield, and the brands riding the wave today are often duct-taping solutions together in real time.

If you’re building in any of these seams, we’d love to learn what you’re seeing. Reach out to us at sophia@equal.vc and chelsea@equal.vc