The Fortune of Failure

The note below was one shared with our team and a select group of LPs on 11/15/2021. Little did we know that the time of this writing would represent the NASDAQ all-time high. While perhaps it’s a bit late to avoid some of the negative consequences of the downturn, we wanted to share in the interest of the lessons that firms and founders can learn from “Equal Ventures’s 5 Principles of Resiliency”.

Equal Ventures’s 5 Principles of Resiliency

Be disciplined to deliver regardless of market

Be well capitalized to seize opportunities when others can’t

Keep some cement in your shoes

Take a long-term viewpoint of fundamental performance

Stuff the mattress

While the market’s downfall has caused a lot of panic, we continue to believe that some of the best companies will be born out of times like these and think these resiliency principles are important to maintain during good times and bad. Whether you are a fund or a founder, building resiliency is essential to ensuring you can navigate market cycles, and the principles outlined above are our best attempt to ensure we do.

Before reading further below, it’s worth noting that the very infrequency of turns in the market cycle is what makes the lessons from them so important. Many investing in or starting companies have never experienced a turn in the market cycle, perhaps leaving them unaware of what it can feel like. In prior cycles like the clean tech bubble and the Global Financial Crisis, I had been a consultant working heavily with PE/VC firms, but was not a lead investor sitting on boards. Nonetheless, being able to see how those investors reacted and the repercussions of those decisions was an invaluable lesson. Similarly, I believe those who experience this cycle will be better equipped to handle future ones. “Smell the air” during times like these to develop awareness of when markets are oscillating between “peak greed” and “peak fear”, and take note of the decisions and their repercussions. It’s in these moments of extremes that careers can be made and/or lost and we’re hopeful that the lessons along can help you and your companies navigate this and future cycles.

Sincerely,

Rick Zullo & the Equal Ventures Team

The Fortune of Failure (written 11/15/2021)

Last night, I was reading Lux’s Capital 2021 Q3 Letter and it struck a chord with me and included some notable commentary and statistics on today’s market dynamics. As always, everything that Lux writes is thought provoking and beautifully written, but this more than most. While I must seem like a broken record, we're in unprecedented economic times and the reality is the flood of capital to the markets has created a new class of investor that has never seen failure. Even amidst a global pandemic, the shock to asset prices was extremely temporary and far more muted than the global financial crisis. >800k deaths later, the markets still continuously test new highs and leverage of retail investors balloons further and further. Despite geopolitical tensions and inflation rising in tandem, the market still continues to see $20b of net flows in monthly. While the market may feel immune to failure (shrugging risk to the wayside), the stark reality is that it simply hasn’t experienced it and that can mean even the smallest disruption have disastrous impacts

The Investor Immune System

Myself, my wife, and 11 month old daughter all lived in New York City when COVID hit in March of 2020. My mother-in-law was recovering from pancreatic cancer and we chose to go to Virginia in case something happened to her amidst the fear that lockdowns could prevent us from seeing her. What we assumed would be just a few weeks or months turned into a year. We lived in a bubble with my in-laws, largely walled off from the rest of society, because my mother-in-law’s post-cancer immune system was so weak. When we were vaccinated, we came back to New York. A year of sterile living had left our immune systems weakened and within the first week we were all sick. Simple colds that would have normally given us a runny nose felt like a disastrous case of the flu. We felt immune to sickness (we were healthy, vaccinated, taking precautions, etc.), but our bodies simply weren’t ready for the influx of germs we were being introduced to. What ended up being a small, immaterial nothing of a cold wiped us all out for a week. Our systems were fragile and a small test sent us reeling.

This serves a potential allegory to today’s investor. More than a decade of stimulus, ZIRP and Fed balance sheet ballooning (combined with arguably some incredible technology achievements as well) has weakened our investor immune system. It’s been so long since we’ve caught a “cold” that we no longer remember what it feels like. This leads the market to edge further and further into risk until even the slightest of nudges can send it cascading off the cliff. Thus far, the government has provided a tremendous amount of immunity to investors, but with stimulus wells becoming increasingly hard to pump up, Fed easing its balance sheet and inflation rising quickly, the immunity that they provide may be waning (fast).

With that, I return to Lux’s piece. The letter doesn’t claim gloom and doom. It doesn’t claim that we’re in the bottom of the 9th of this latest cycle. It doesn’t claim the end of days for financial markets. For that matter, neither do I. That said, it recognizes the importance of knowing where we are in the market cycle and acknowledging the environment we are in. This is why knowing what failure feels like is so critical. I’ve often told our LPs that we need to “smell the air” of this market environment to know what it’s like for the next cycle we experience in our career when we’ll have far more chips on the table. Arguably just as important is knowing the stench of market failure and that’s something few in today’s climate have ever dealt with.

I’ve experienced market failures twice in my career. On my second assignment at Deloitte, I was tasked on a contract with the FDIC. My manager thought it would be a good way for me to get some financial analysis / M&A experience (given my long-term interest in PE/VC) and the contract was local, so I was a cheap resource. Our job: coordinating the receivership and sale of failed banks to other larger banks who would absorb those assets to ensure continuity of the banking system. My friends from college gave me a hard time because I was doing a banker’s work with banker’s hours but making less than half their compensation. Our focus was initially small, regional banks, however, this accelerated and before long we were informed that a bank far too big for our traditional playbook was going to fail…Lehman Brothers. At that point, we knew the market would tank and were absolutely powerless against it. What ultimately became “too big to fail” wasn’t in place in time to protect the economy against one of the largest defaults in American history.

After several weeks working north of 100 hours, I rolled off the project and was fortunate to get staffed on some work in the energy space. I had joined Deloitte under the wing of one of the firm’s global leaders in the energy space (who remains a close friend today) and was fortunate to have a front row seat for the first cleantech wave, ranging from working for the Department of Energy, various power & utilities clients, EV manufacturers, PE/VC firms and international development organization alike. I got the chance to work on some incredibly exciting projects and started to see a flurry of requests from headhunters targeting me for PE/VC jobs (candidly, I didn’t even understand the difference between the two at the time). Then all of a sudden, it stopped. I remember exactly where I was (the LA Fitness in Foggy Bottom, DC) when Harry Reid announced that they were deprioritizing climate tech legislation (which had bipartisan support) for the Affordable Care Act. The promise of cleantech, which itself had been propped up by government stimulus and subsidies at the time, immediately deflated. Job prospects eroded and calls from headhunters evaporated. I became unmarketable. I removed mentions of energy from my resume, repositioning “cleantech” as “high tech” and managed to score a few interviews. In one interview with a prominent VC firm, the response from the Partner interviewing me when he finally realized that my background was in “cleantech” was priceless “Ewww…I’m sorry about that.” (true story)

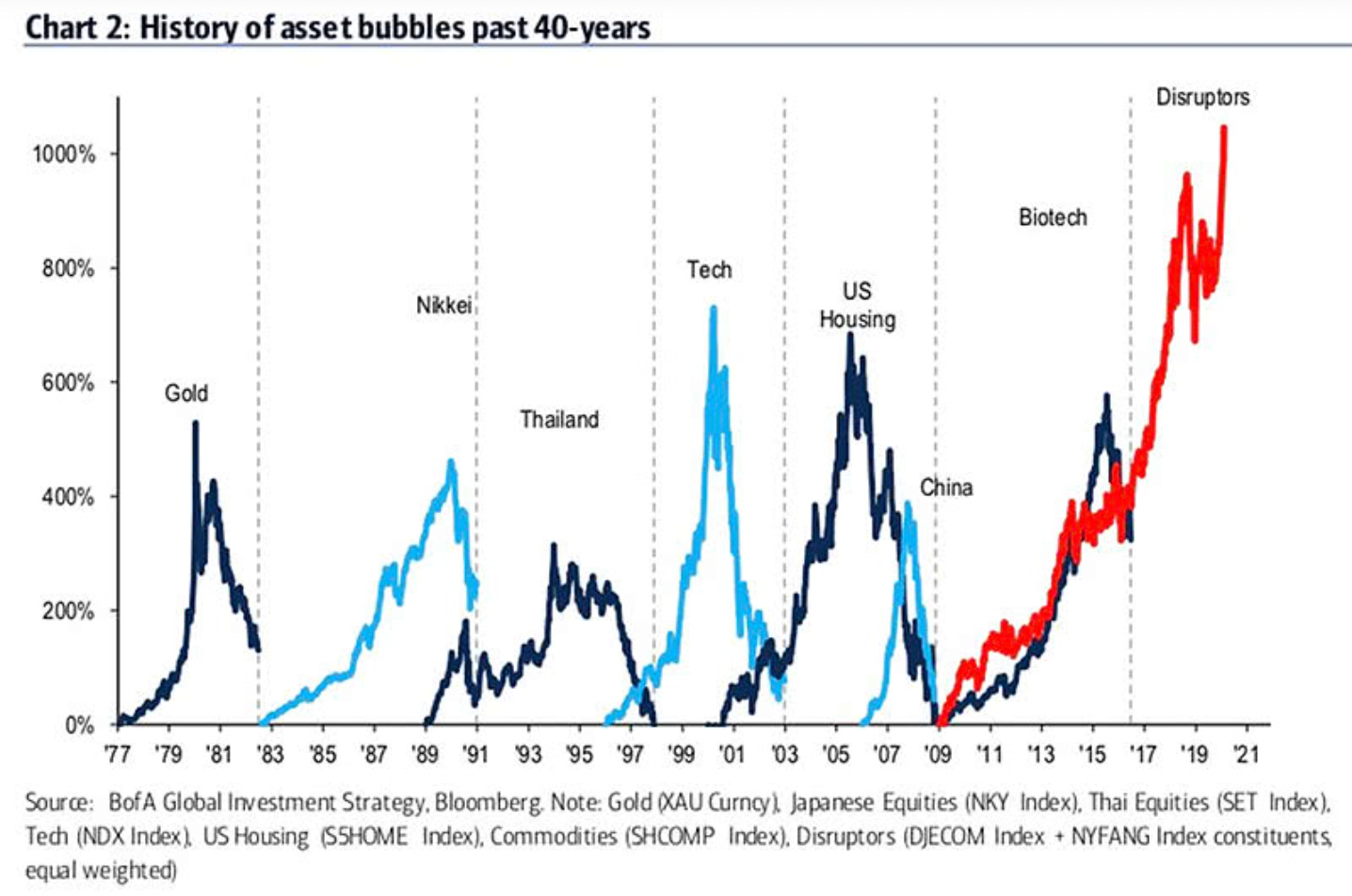

The Case for a “Bubble”

In each of these cases, we saw market hubris tilt beyond financial reason, we saw government propping beyond what they could support and investors investing in new asset categories they fundamentally didn’t understand (whether it be CDOs or carbon sequestration). In Boom and Bust: A global history of financial bubbles, Quinn and Turner outline the three factors present to enact a bubble; they call it the “Bubble Triangle,” a framework based on the ‘fire triangle' of oxygen, fuel, and heat. When each element is present, a fire can be started by a simple spark. In the case of the Bubble Triangle, a single political or technological event can spark the fire that fuels the bubble, provided that you have three conditions:

Marketability of securities

Ample access to money/credit

Promise of speculation for a technology advancement

Arguably, these three principles are more in place today than they were during either of the previous bubbles. Investors can buy fractional shares of stocks, crypto currencies and virtually anything else you can put your mind to regardless of how small the denomination is. Retail leverage is as high as it's ever been, the Fed balance sheet is 10x what it was pre-GFC and interest rates are as low as they have ever been in the course of human history. Yes, we’ve seen a tremendous wave of technology innovation and one that our own firm has benefited from greatly. Digital transformation is indeed happening at a rate beyond what I have ever seen in my professional career. This is creating tremendous belief in the future value of technologies across the board, not just software or AI, but blockchain/crypto, climate tech and flying cars. David Faber from CNBC quipped on SPAC projections “2026 seems like it's going to be a big year”.

Marketability, check. Money/Credit, check. Speculation, check. The conditions are in place and COVID was likely the spark that sent a buoyant market into an all-out bubble. Equity values are at historical valuation multiples for virtually every logical test (here, here, here). The only safe haven framework is highly leveraged to interest rates which could rise dramatically in coming months (here). For SaaS valuations, despite a 1/3 pullback in forward revenue multiples, current multiples are more than double their historical value (here). A mentor of mine (a prominent VC for over 20 years) once told me his take on market cycles and bubbles. I asked him “Do you feel this time it's different?” His response, “Every time they feel different, every time you get the same result.”

The greatest trick a bubble plays is convincing us that this time it’s different. Even prior to the Great Depression, society (and investors) had convinced themselves of “modernism” with a shared belief that technology innovations (primarily driven by oil, consumer auto and mass production) completely changed the rules of economic value and historical measures like cash flow were no longer relevant. Time has tested this and market cycles are more persistent than gravity.

The conditions and the proof points are there, the question is what will make the bubble pop and what will you/we do to navigate the cycle. I don’t know when and what will pop the bubble and whether it will be a violent downturn (as the last three bubbles proved to be – 1) internet, 2) GFC and 3) cleantech) or whether it will be a more muted relief like that we have seen in the past. That said, I’m glad that I’ve experienced market failures before as we prepare for whenever this one does come.

Principles of Resiliency

The fortune of failure belongs to those who wear the wounds of these past market cycles. I, for one, have certainly been more risk averse during these last couple of years, pricing in the potential for downside risk. Others have made tremendous money/returns with the “risk on” trade and I applaud them for it. Risk-on will always out-perform in a bull market, but (for better or worse) I’ve aligned on a viewpoint to position myself to manage through market cycles. This means, taking defensive steps even when others are being as aggressive as possible. Not all of these can be encapsulated in a single lesson, but here are a few of the ways I continue to think about positioning ourselves and our companies through those turns:

Equal Ventures’s 5 Principles of Resiliency

Be disciplined to deliver regardless of market

One of our LPs often notes “Just because you can, doesn’t mean you should”. As LP capital becomes more available, there is a rush to accumulate as much AUM as possible, often at the detriment of returns. The fees are incredibly beneficial to GPs in the short-term, but the added pressure of putting continuously more money to work quickly leads to strategy diversion and misalignment of interest. If/when markets wane, putting excess supply of capital into a scarcer set of opportunities could lead these funds to some difficult pastures. Personally, I’d rather position ourselves to leave the fees on the table, but capable of delivering through good times AND bad.

Be well capitalized to seize opportunities when others can’t

While this may seem in direct contrast to #1, it’s not. Positioning ourselves as investors to have the liquidity to invest when markets are at their most skittish, may present the greatest opportunities. As Buffet says, “Be fearful when others are greedy, be greedy when others are fearful.” This requires consistency of capital providers to ensure that regardless of how the market turns, that you will have the liquidity to execute. This is where the quality of our partners (i.e. LPs) and the quality of those relationships truly matter. The last thing a fund manager should want to do is fundraise as a market is turning sour and if the quality of the LP and/or relationship are not sound, those managers not only risk missing out on opportunities, but rather their firm’s survival.

Keep some cement in your shoes

While I’m proud of our performance, we are beneficiaries of market conditions that may not always be present. We must remain as humble, as disciplined and as diligent as ever to maintain our performance and avoid the urge to pat ourselves on the back too early. This mentality will reward us regardless of market cycles.

Take a long-term viewpoint of fundamental performance

Don’t chase artificial multiples propped up by current market conditions, but rather ask yourself “Is this a company that will perform regardless of market cycles and generate an amazing return even in a bad market over a 10 year time horizon?” I’ve seen this thinking infiltrate my own mind (chasing multiples for near-term mark-ups) and am forced to remind myself that near-term multiples don’t matter, but the long-term DCF does.

Stuff the mattress

Making sure our companies are fully capitalized to survive and thrive through the market cycle is one of the best ways we can position them to use the market’s swing to their favor rather than their peril. This capital will enable them to play offense when their competitors are busy treading water.

Closing Thoughts

As Warren Buffet famously said “Only when the tide goes out do you discover who's been swimming naked”. We’ve intended to build our firm to be resilient regardless of the tide and believe these measures will help us do so. I don’t know when tides will turn, but I’m hopeful that the lessons that we have learned from previous failures have strengthened our immunity to the potential downside ahead (keeping us somewhat clothed as the tide goes out). With that, I’m confident as we march forward into uncertainty. I’m confident our portfolio can outperform in any market. I’m confident our approach can outperform in any market. Lastly, I’m confident our team can outperform in any market. My hope is that we’ve built our firm with the intention of resiliency to these cycles. Like all others, we’ll be negatively impacted when cycles turn, but my hope is that the decisions we have made will soften these impacts to a minor cold, rather than a fatal flu. Adhering to our mission, our thesis, and our values as a team are at the core of that and I’m confident that these can position us for success regardless of any cycle.

*Read this on Medium here

**Read more on Twitter here