The Great Climate Tech Debate – “Digital” or “Frontier”?

*Engage with this post on Twitter here

I’ve spent most of my life working on two core areas – 1) clean energy and 2) digital transformation of legacy sectors. The first 5-7 years of my career were explicitly focused on the former. I interned for NGOs and in the sustainability division of a Fortune 100 company before graduating college in 2007 and then joined Deloitte where I had the pleasure of working with clients across the public and private sectors in the early days of “cleantech.” I saw billions of dollars of capital deployed into promising cleantech solutions, worked with utilities and large scale corporates to evaluate, commercialize and deploy these technologies and spent significant time abroad doing the same.

Shortly before business school (in 2012) I moved to a small tech buyout fund to transition sectors. To say that the cleantech market was ice cold would be an understatement. I continued to look at investment opportunities where my knowledge of the energy space was relevant, but I made a decided effort to focus on software/tech moving forward.

10+ years later, I’ve had the chance to align these two worlds together as “cleantech” has shifted to “climatetech.” Our team has done a tremendous amount of research to pick the spots where we want to play, leveraging a deep network of experts and operators in the field (NOTE: not just academics, people who actually deploy and use these tools everyday). We partner with these folks as change agents (we refer to them as “bridgers” – those capable of bridging the divide between startups and the real world), and consider ourselves extremely fortunate to have their perspective.

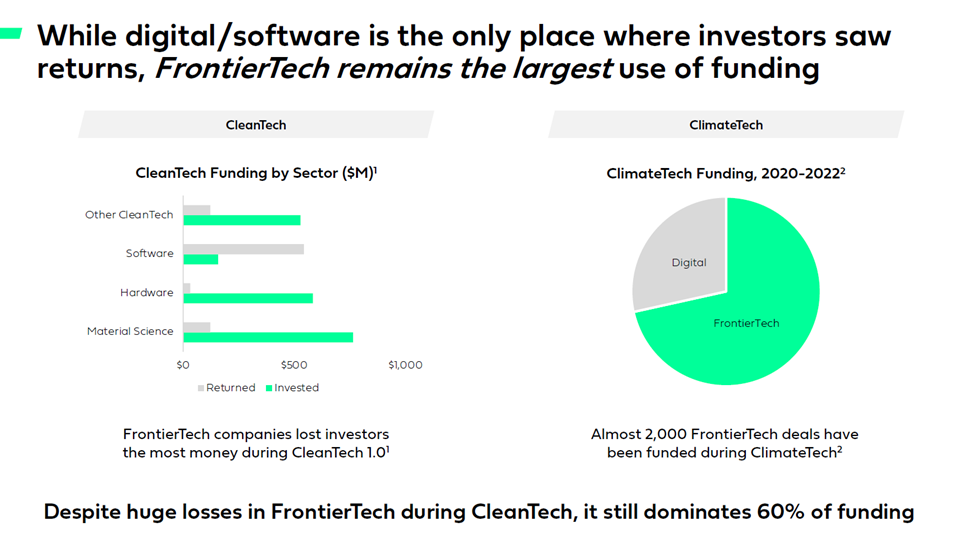

Amidst all of this, we see a tremendous amount of investment activity in “climatetech,” particularly in frontier markets and hardware. These areas have been the dominant beneficiaries of climatetech funding with the ambition of producing and commercializing novel technology in markets like nuclear and carbon capture. Meanwhile, digital adoption in the energy sector remains criminally underinvested. Investors say “selling into utilities and building is too hard” and they are right, but selling into a commodity market (power, credits, carbon, etc.) that requires hundreds of millions of asset deployment at negative gross margins before your first dollar of revenue isn’t easy either.

Capital Flow & Returns - Digital vs Frontier

Through our research, we learned that even amidst the bloodbath of the “cleantech” bubble, there were pockets where money was made. Turns out that digital investments returned close to 3x the capital invested, whereas investments into hardware and material science lost 80-95% on the dollar. One would think that we/VCs would learn from this lesson, but VCs have continued to plow money into frontier investments, while leaving digital in the dust.

Frontier Investing in the Cleantech Bubble

As we looked at successes and failures of the cleantech bubble, a clear trend emerged. The biggest losses were capital-intensive frontier technology companies producing new forms of generation, storage and fuel. These were companies promising innovation that they had discovered scientifically, but with the hope of making money by either 1) manufacturing and selling their innovations to enterprise customers/users or 2) leveraging that technology to yield an advantage in producing fuels or power that they would sell into the broader market.

These companies broadly failed, with more than 90% failing to return even the initial capital invested thanks to troubles building out manufacturing/production centers (the capabilities of a scientist may be different than that of someone leading the design and development of a factory). Most of the technology gains that were discovered in the labs were either far less effective or far more expensive than initially promised. This was amplified by US-based manufacturing (which was a contingency of the DOE funds leveraged by these companies), where construction delays enabled foreign-based competitors to fast-follow technology and scale quicker with far lower costs.

Fundamentally this comes down to the core competencies required to win. Dan Wang summarized this dynamic well, saying “China's focus on manufacturing sometimes beats America's focus on science. The US laid the scientific groundwork in the solar industry, for example, only for China to build all the panels. The US must relearn scaling.” Selling panels into the market didn’t come down to technology advantage, it became about manufacturing scale advantages – something that few US startups have any expertise in. This further complicated the slope of the falling cost curves. With this, even a full 1 year technology lead on competitors could quickly be eroded by production delays or by the speed of larger players who could repurpose existing manufacturing infrastructure. Furthermore, the slope of these curves created a dynamic where the technologies were becoming obsolete by the very time they finally came to production.

Ultimately, those who survived in this space (companies like First Solar) recognized that the manufacturing of panels was becoming commoditized and that they needed to own their distribution channel to win. These manufacturers became developers in their own right as a way to drive greater throughput on their production and achieve economies of scale. Ultimately, it’s not the technology that is making First Solar win, it’s 20 years of operational execution, asset-based verticalization and economies of scale. Generally speaking, those are not the core competencies of early-stage, frontier tech startups, which is why it may not be a coincidence that First Solar was never backed by venture capital.

Digital Investing in the Cleantech Bubble

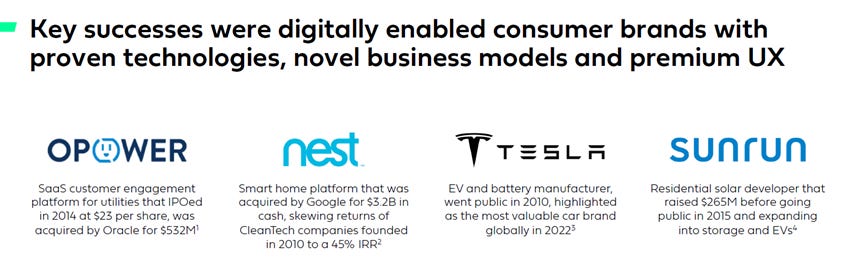

The key successes of the cleantech bubble follow a decidedly different arc. These companies (like those listed below) far more closely resemble the core competencies that VCs are used to evaluating and advising. They created digital and/or consumer products that won on customer experience and business model. None of these companies (even Nest or Tesla) were developing frontier tech, they were leveraging existing technology and repackaging it into a superior UX that made it digestible to consumers. Players like Sunrun and Tesla were able to capitalize on what the others had done to lower the costs of panels and batteries, while focusing on other core competencies to drive their competitive advantages. Companies like Nest and oPower, were able to unlock consumer behavior with their superior experiences, much like how Tesla was able to make electric vehicles cool with the car’s design and Elon’s rockstar persona. Sunrun leveraged digital solutions and data science to identify and qualify high-likelihood customers, dramatically cutting the soft costs (which can represent over 60% of the total cost of a solar project) for homeowners.

Some frontier tech advocates would contend that Tesla belongs in the former category, however it’s widely known that it was Tesla’s foray into manufacturing that nearly killed the company. Elon had to co-lead a $40m bridge to save the company after most of his investors walked away. Even then, Tesla was only a $2b company when it went public and its share price barely budged for the first 3 years as a public company. It’s seen tremendous appreciation since then, but any core competitive advantages the company has benefited from are those that it’s developed over the course of being a public company, not as a startup. The gains for investors align with this, with the vast majority of returns coming a decade AFTER it went public. As a public investor in Tesla shares in early 2013 (3 years after going public), you’d see a 100x return based on the current share price. VC investors (who largely sell within the first year of a company going public) would have seen something far smaller. Below is a chart of Tesla’s share price over its 13 year history as a public company - I’ll let you come to your own conclusions on who the winners are :)

The Role of Venture Capital

Regardless of the Tesla debate, it’s clear that focusing on the core strengths of digital experience, brand and business model is what produced the winners of the cleantech age. This is also where VCs are best positioned to evaluate and advise emerging companies. Working with many emerging technology companies and investors during the initial cleantech wave, I can safely say that many promising innovations were destroyed by uninformed investors chasing the momentum of the category. These investors advised companies to follow the best practices they had learned as software and consumer investors, but the tactics and playbooks necessary to win in a market that required manufacturing and scaling expertise were wholly different. A lot of this was justified as “Well, these are really smart people, so they can figure it out,” but I don’t think the venture community would provide the same leeway to a hedge fund manager or nuclear scientist (both of which are undeniably very smart) investing in a seed stage SaaS company. Far more likely, they would say, “What do those folks think they are doing? What do they know about building a SaaS startup?” My job as an investor in seed stage digital companies isn’t easy, but I’m pretty certain it's easier to evaluate and build a SaaS company than it is a modular nuclear reactor.

That’s not to say that I don’t find these technology innovations interesting or the need for “bits and atoms” investing necessary – I do! That said, the question is whether it’s VC’s role to play in the process. We are, after all, not the ONLY form of capital (we’re actually a very small sliver of the overall capital spectrum). Many of these technologies will take over a decade to bring to market from where they are today, whereas VCs typically have fund cycles that require them to return capital within a decade (firms like Breakthrough have longer fund cycles and I think are well positioned to invest in these types of companies). Tremendous research happens out of the DOE’s national labs and the grants it provides to university research centers. My sense is that these are the deep pocketed, long-term minded players that will win (the talent at these labs is incredible) and that will provide the opportunity for entrepreneurially-minded companies (founders and incumbents) to commercialize their work with novel business models, superior delivery and best-in-class manufacturing expertise.

History does not repeat itself, but it does rhyme

Mark Twain once said “History does not repeat itself, but it does rhyme.” I firmly believe that learning from our past is one of the finest ways to position ourselves for the future and the corollaries that I see between today and my initial years in cleantech are stark (we will expand upon these in a future post). I can’t forecast what will happen in the future, but the results of the cleantech bubble are facts. What we’ve tried to do above is explain why those results came to be by analyzing the market conditions and competitive dynamics of the energy industry. Our job isn’t to tell founders or investors where to spend their time, but as someone who has devoted an immense amount of his life to the progression of climate solutions, I feel it’s important that others choosing to follow that path should have the opportunity to learn from the lessons of the past to make the best decisions they can about the future. When it comes down to climate, it’s just too damn important.

While there are parts of the ecosystem that concern me, I’ve never been more optimistic about the potential for true climate progress. My belief (as someone who has worked across various facets of the industry locally vs. abroad, public sector vs. private sector, supply vs. demand, asset-based vs. technology), is that much of the bottleneck of climate progress is related to misalignment of incentives and inefficiencies that can easily be solved with off-the-shelf software and hardware solutions. Again, that doesn’t mean that there isn’t a role for breakthrough technology innovation to take place. I strongly believe this is a critical part of the portfolio of solutions required to address our needs, but I know tremendous progress can be made today on the tools we already have in place. Software can have scalable impact at TREMENDOUS speed and that’s what we need - action TODAY. I’ve seen the impact of clean cookstoves, residential solar and basic energy efficiency measures in some of the most impoverished places in the world - unlocking their potential would have amazing impact. At the other end of the spectrum, I can look to the energy riches we have here in America and see us consistently squandering our resources (despite growing idealism) because of breakdowns in incentives and information flows. There is SO much opportunity for investment in these areas and the impact that could be generated would be both immediate and radical.

The energy sector, despite its tremendous size, remains one of the biggest digital laggards across industries. We’re seeing tremendous economic and environmental progress with digital solutions like David Energy and Odyssey Energy Solutions, and believe there are many other digital opportunities that represent the chance for significant returns. It’s possible that frontier technologies can break from the track record of the past and produce great returns for their investors too, but we would surmise that investors position their firms with the capabilities to serve those founders (deep technology understanding AND experience rapidly scaling manufacturing at low cost) rather than relying on the skill sets that made them successful elsewhere.

We have some exciting years ahead in technology’s pursuit of climate progress and we’re hopeful that more founders and investors will join us in the mission of digital transformation of the sector.

*Read this on Medium here