What Matters Most: How We Develop Conviction at Seed

In a recent conversation I had with a founder looking for some friendly advice, he asked “what metrics do I need for a seed round?”. I get this question a LOT and it always frustrates me a bit. To distill the total worth of a company to a few basic metrics has always felt limiting, especially when the value of the company is what it will do in the future, not in the past. For better or worse, I don’t focus on metrics at seed and I personally don’t know why others do.

This opens the larger question of “how do you develop conviction?”, so I thought I’d provide some additional clarity. While every company is different (in turn, our process for evaluating that company is unique to that company), uniformly there are 4 things we like to for a “Equal Ventures” company prior to investing: 1) “moat trajectory”, 2) proximity to product-market fit, 3) “why now?” and 4) team.

Moat Trajectory

The first of these is probably the most specific to Equal. A big part of our belief in transforming legacy markets is understanding the economics of those industries and determining the opportunity for the company to carve out a “moat” in that industry’s value chain. While companies never have a moat on Day One, we try to evaluate their “moat trajectory”, which is the long-term sustainable advantage they can have over competitors IF everything goes according to plan. Generally this means the company has the ability to monopolize a segment of the value chain and sustain it given a flywheel inherent in their business model.

Generally speaking, we want to see the ability to monopolize a $1b+ segment of TAM (margin, not revenue). We can get comfortable with smaller TAM segments provided that 1) there is a near-term path to achieving that (will discuss this shortly) and 2) we believe the segment lends itself well to monopolization, rather than many players.

Ultimately, we want companies capable of generating long term FCF, and that requires a defensible moat position in the market, not a leaky bucket with lots of revenue.

Proximity to Product-Market Fit (PMF)

Product-Market Fit can have a relatively squishy definition for some, but for us, it’s pretty clear. We see PMF as the first demonstrations of 1) increasing returns to scale (aka a flywheel) that 2) enables a path toward a moat trajectory. We need both. Increasing returns to scale that don’t lead to a potential moat, don’t matter. We’ve seen this with companies that demonstrate customer network effects accumulating large audiences, but are ultimately unable to successfully monetize or take their stake in the value chain. Value creation without value capture makes for great altruism, but bad business. That said, if we see a flywheel in place with a path toward a moat, we know that (given sufficient capital and quality execution) the company has the potential to develop a sustainable business.

Given where we sit in the investing landscape, we want to invest with near-term visibility (6-12 months) of that PMF inflection point. At the end of the day, we see our seed capital as a means to validate or disprove a hypothesis on proving PMF. Sometimes companies have a product beforehand, sometimes they don’t. Either way, we want to know that our capital is going to be sufficient to run that experiment. If successful, we know we’re ready to raise follow-on funding. If not, having a shorter time horizon gives us the opportunity to pivot. Either way, we don’t like to be sitting on our hands too long, so we want to know that we’ll be collecting data for the experiment shortly after investing. This generally keeps us out of companies with long, extensive build lifecycles like hardware, but we think that’s the right strategy for our firm based on where we sit in the investment spectrum and the capabilities we have around the table.

Why Now?

Someone once told me that “Alpha = Perception - Reality”. Forgive me, I can’t remember who said this (we’ll update the post if someone can claim it), but I think this is a really insightful way to think about efficient markets.

Building a startup is highly competitive. When markets are stable and mature they are incredibly difficult to change. A new upstart rarely has a chance if it’s competing with titans on their own turf. Great companies, however, see opportunities before the broader market recognizes them. They see a catalyst open the door for opportunity, determine how it creates a new need in the market for them to exploit and sprint to fill it with the hard work of amazing people. They turn the unseen edge of a market into the widely accepted reality. Finding that opportunity before it’s obvious is where the alpha exists.

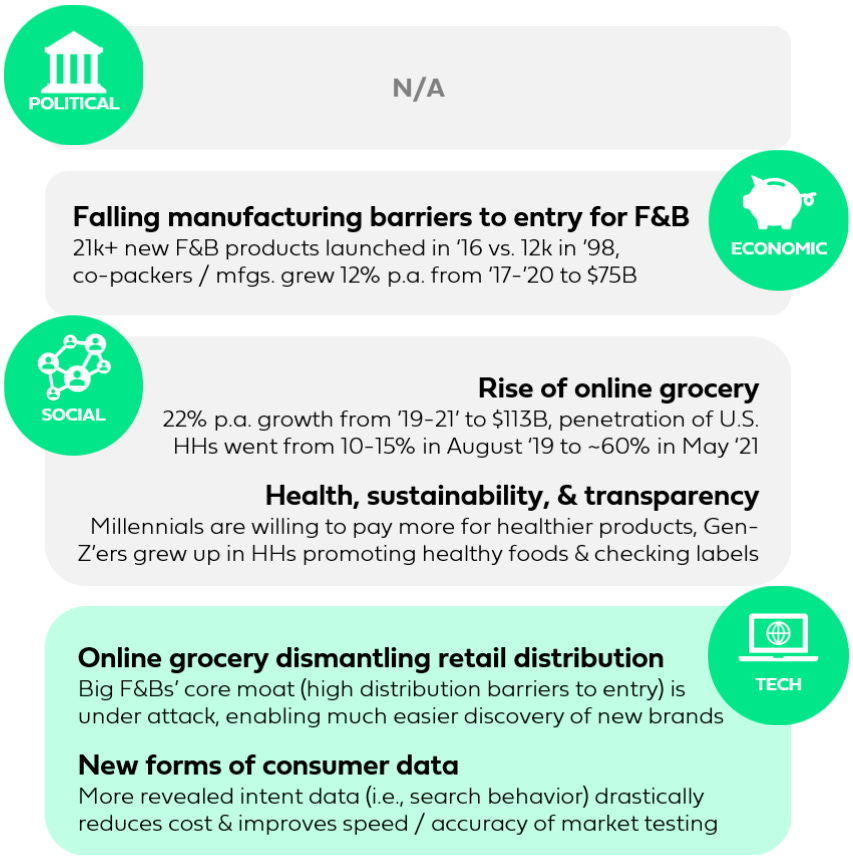

This is why we ask “why now?”, or said more precisely, “what is the catalyst that creates an opportunity for this business to exist in ways it previously couldn’t?” We leverage the PEST framework (which focuses on Political, Economic, Social and Technological conditions) as a starting point for this evaluation, but often consider outside considerations as well (see an illustrative example below for our portfolio company Starday Foods)

Example PEST Analysis for Starday Foods

The “why now?” helps us align with the founder(s) on why there is an opportunity in the market that previously didn’t exist, while also informing the future strategy of the business. Legacy companies are often optimized on previous conditions, turning what were once competitive advantages into massive liabilities on the business. Upstarts can position themselves around new market conditions, investing to develop competitive advantage in the new world order as the goliaths attempt to figure out which course of action to take. This agility is one of the core advantages of being a start-up, enabling them to exploit market timing in ways that bigger players can not.

Team

This is the most important of the three and often takes the longest to properly evaluate. We can do our work on a market before meeting with a company to understand potential moat trajectories (and we do). Similarly, we can discuss an operating plan for the next 12 months and get a sense of whether the company is going to be able to effectively test for PMF in that time frame.

First and foremost, when we look at teams, I do NOT care about your pedigree. I care about YOU, not where you went to school, whether you had a killer score on a test or if you are connected to other VCs. In my opinion, these are all constructs that VCs have placed on founders to fast track team evaluation in sake of “pattern recognition” that dangerously reinforce bias. This leads most VCs to look for founder archetypes and signs of external validation (ex. degree from Stanford, YC or experience at well regarded startups), rather than use their own independent judgment to determine whether this is the right specific team for this specific opportunity.

We choose to focus on qualities > pedigree. When evaluating founders, I like to see 1) grit, 2) decision making ability, 3) drive for self-improvement, 4) their ability to attract/retain/develop the BEST talent and 5) founder-market fit. Determining a founder’s strengths in these areas is a System 2 function and it takes real time to properly see the person for who they are, not just their profile. I love that process and it provides a great opportunity to build a relationship for what could be a 10 year partnership. Our #1 job as investors is to get the “team” part right, so it’s no surprise that we spend a tremendous amount of attention evaluating this as part of our process.

How We Make Decisions

These are just a few of the major driving criteria for how we develop conviction at the earliest stages of a company. To provide full transparency, I’ve included our “initial preliminary vote” form that our team uses to provide feedback on a deal. We don’t tabulate scores to determine whether to invest, but use this as a means to collect valuable feedback from team members (everyone on our team fills it out, not just myself and Rich). Much like with ourselves and our founders, this form strives for continuous improvement so it always changes. That said, note that nowhere in here do we talk about metrics or pedigrees. Our process will change and (hopefully) improve over time as well, but I believe we’ll adhere to similar principles and we’ll try to provide as much transparency as we can on what matters to us. I’m hopeful that this transparency is helpful in better understanding Equal as a firm, as founders look to partner with us on your journey to transforming legacy markets.

*Read this on Medium here

**Read more on Twitter here