Concentration > Diversification

In today’s market, stiff competition and heightened market valuations are raising concerns across the venture ecosystem. Many fear that consensus returns for this period could ultimately be mediocre and see a reshuffling of both the venture hierarchy and the way venture as an asset class operates. With that, figuring out an advantage over the consensus is more important than ever - it’s not just a means to returns, it’s a means to survival. Some believe that power law dynamics suggest a capital cannon approach to lay down as many bets as possible in the hopes of achieving a $100b outcome (which is now more possible than ever) that will justify many losers and, to be fair, they could be right. For better or worse, that’s not me and that’s not Equal Ventures.

When we started this firm, one of our core ethos was “concentration > diversification” and that was for two reasons: 1) we felt that was a far better experience for the founder and 2) we felt that it was our greatest chance of generating incredible returns for our LPs. To be clear, this strategy is terrifying. We are investing in companies that have virtually NO data, that we have NO control of and are taking a limited amount of shots on net (less than 20 in Fund 1). We lead pretty much every deal we do but we often have limited visibility as to whether the market will find the opportunity attractive or not. The average startup failure rate is 90%, with 50% failing in their first five years. This suggests we could see only 10 companies make it past Series B and even fewer making it to a long-term liquidity event. That is a TREMENDOUS amount of risk to put into what could be a very small basket (fortunately our historical portfolio has a significantly higher survival rate).

That said, this model can drive massive returns. We’ve seen this with funds that have remained disciplined in fund size and have produced epic outcomes such as Union Square Ventures, Benchmark Capital, Emergence Capital, IA Ventures and Pivot North (amongst others). Some of these names aren’t as well known as the multi-stage players on Sand Hill Road (or I guess, South Park these days), but if you ask LPs, these are ALL legendary funds. These firms vary in stage and approach, but share two common threads - discipline and concentration. Partners at these firms may do 1-3 deals a year (compared to Tiger Global's deal a day pace). Fred Wilson, perhaps the best investor of all-time, went all of 2012 without doing a single investment. There are many ways to drive returns for LPs, but these firms demonstrate that disciplined fund size with concentrated bets is one way to achieve them.

Perhaps more important, however, is the impact this has on founders. As capital has become increasingly commoditized and fundraises turn to auctions, we lose sight of the relationship between founders and VCs. That is my single favorite part of this business. Some of my founder relationships are the closest relationships in my life. And before you say that’s sad, I’ll tell you that I love it. I get to show up to work everyday and help some of my best friends solve problems that can change the world - that’s pretty cool. We celebrate the wins together and we can be the shoulders to cry on during the hard times - as sappy as that sounds, it’s extremely rewarding. But we’re not just cheerleaders patting them on the back, we pride ourselves on 1) understanding their space just as well as any other investor out there, 2) being aligned with them to give them an unbiased POV on how to maximize shareholder value and 3) supporting them with hands-on support in a way that other VCs can’t. We write our values on our website and live them day in and day out, because we think they help make us the trusted advisor to the CEO. They help us push when they need to be pushed (telling a founder what they need to hear, not necessarily what they want to), because there is a level of trust and respect that is different from simply a capital allocation mindset. Our concentration enables us to offer this product and we feel it becomes increasingly differentiated in a market where most are accelerating pace to a level that makes it impossible to work with founders on a day-to-day basis. Some founders don’t value that (and we generally get obliterated on price for those companies), but for those that do, we think it provides meaningful alpha to our LPs by getting preferred entry points and by playing a meaningful role in improving a company’s chance for success. I know we can’t “Out Tiger, Tiger”, so we need to 1) find the opportunities that they can’t (or don’t find compelling) and 2) serve a product to founders that is different. For me, that is concentration.

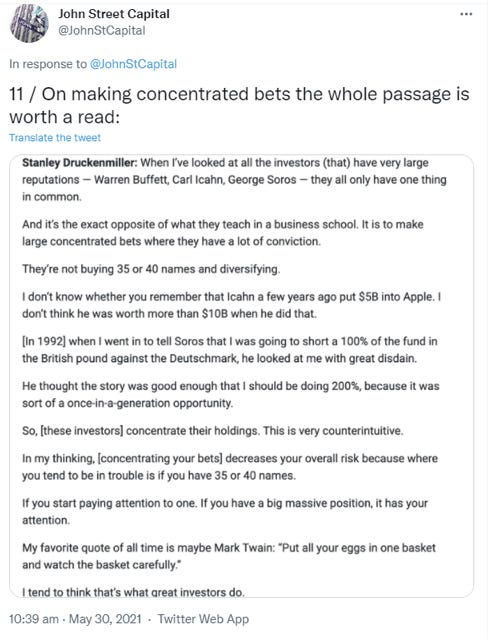

For many, the path to concentration is intimidating and it doesn’t happen overnight. Our friend Kanyi from Kindred Ventures noted this in a recent tweet that sparked some great conversations on Twitter.

Given how risky this strategy is, Kanyi is right. Most up and coming investors don’t get the latitude to make concentrated bets, let alone in something as crazy as early-stage venture. For me, I grew up in concentrated bets. I started at a PE fund that might do a deal a year and when I landed in venture, I was working at firms where my pacing was 2-3 deals per year. If I wanted to take a shot on net, I had better be damn sure it was going to be a slam dunk. Concentration necessitates a higher degree of conviction, which forced me to develop theses, track down deals in uncharted waters and identify opportunities where I had asymmetric information. This wasn’t intentional, this is what I had to do – this was the only way for me to be a VC given the roles I was in. After 9 years of investing in tech companies, I can’t imagine investing another way.

Again, there are numerous ways to operate as a VC. My hope is that ours is one that leaves both our LPs and our founders feeling very happy about their relationship with Equal Ventures. Knowing what your “product” is in this landscape is just as important as anything else and I know I can’t compete with most funds on capital allocation, speed or price. Where I can compete is on concentration, preparation and perspiration. With that, I’m hopeful (and perhaps optimistic) of the decade-long relationships we will forge with founders in the years to come to help them transform their industries.

For those looking to learn more on concentration, here is a parting note from @johnstreetcapital that Kanyi referenced with a transcript from legendary investor Stanley Druckenmiller.