The Equal Ventures Insurance Index

Q3 2025

Follow the conversation on LinkedIn

The Equal Ventures Insurance Index is a quarterly summary of market performance and trends in P&C insurance. The indices we report include public equities from insurance and insurtech, from which we draw insights about key themes affecting the sector. This post summarizes the performance of our indicies in Q3 2025 and the first weeks of Q4. As always, our goal from this post is to help support observers of the insurance industry in identifying trends and catalysts that affect the P&C industry (and never to recommend any specific investments).

In many ways, Q3 was a continuation and acceleration of themes from Q2, with carriers and brokers in our indicies pointing to slowing (or contracting) rate growth. Healthy combined ratios and availabilty of reinsurance capacity are driving competion higher as rates trend lower. While profitability is still generally strong, lower growth and the increasing possibility of slowing macro led P&C indicies to underperform the broader (quite strong) equity market. Follow below for our takeaways from Q3 2025.

Q3 2025 Index Summary & Highlights:

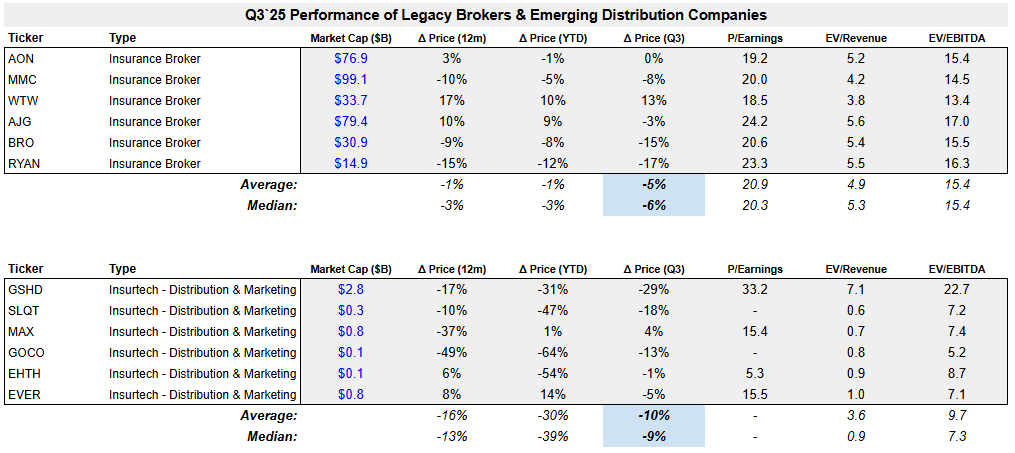

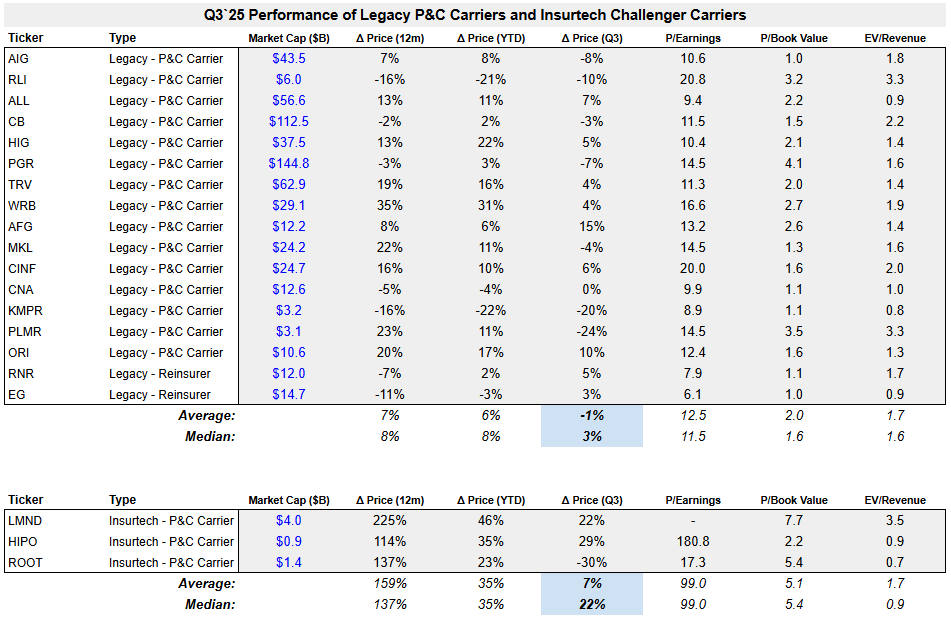

P&C stocks generally underperformed the strong equity market in Q3. Legacy brokers in our index fell by a median of 6% and carriers were up by 3%, compared to SPX +8%

Insurtech carriers (once again) outperformed on average, though the group showed more dispersion in prices across companies.

Light natural catastrophe activity supported strong reinsurance performance, but also accelerated softness in rates, with property rates down 8% q/q.

If there were a single overarching theme to explain P&C performance in Q3, it would be increasing competition and lower rates.

The Marsh Global Insurance Market Index showed commercial rates fell 4% on average in Q3, following a 4% decline in Q2. Again, rates were led lower by property (-8%). Casualty rates remain positive but decelerated Q/Q. As Marsh’s CEO John Doyle said in the company’s Q3 earnings call, “It’s a competitive market.” Insurer ROE remains “quite strong” prompting carriers to look for growth and undercut on pricing, even amid signs the economy is slowing. Doyle pointed to the “unsustainable” mismatch between softening rates and the rising structual “costs of risk,” including extreme weather events and social inflation, which are “increasing at a rate much higher than GDP.” Over the long term, he concludes that more complex risks will be good for the brokerage and risk consulting business (as they may drive rates higher and make consultative expertise more important). But in Q3, the trend toward softer rates hit the sector hard.

Legacy brokers in our index were down by a median of 6% in Q3. Brown & Brown (BRO, -15%), the 6th largest US broker, is a case in point. The company reported substantial renewals in its property segment during the quarter, and rate declines pushed organic growth lower, leading the stock to get crushed in its July earnings. Commentary on the call was that E&S rates were down as much as 15-30% in some segments— an acceleration to the trend that was already worsening in the prior quarter.

The story was similar for legacy carriers, which traded modestly higher on the quarter but underperformed the SPX by close to 500bps. Kemper (KMPR, -20%) led the carrier index lower on similar rate pressures. Their Q2 report in August showed deceleration in policies in force, and they posted adverse loss developments that they attributed to “large losses” and social inflation. Asked about the competitive environment on their earnings call, their CEO assured analysts that they are not “putting on the breaks” in response to softening rates, but also reminded listeners that “the double-digit growth that folks experienced over the last 1.5 years” were not normal or sustainable long term. The growth narrative definitely feels different from a year ago.

While softening rates led by property were already in motion throughout 1H, it is important to note that Q3 also turned out to be an unexpectedly light quarter for seasonal natural catastrophe losses. Catastrophe bonds and reinsurance capital were at record highs and the hurricane season was expected to be intense, but turned out to be much more modest than feared heading in Q3. Though this is great news for reinsurers and for property owners/residents in storm-prone and coastal areas, it may also continue to put pressure on the trajectory of property rates. RenaissanceRe (RNR, +5%) remarked on their earnings call that “this year has gone exceptionally well with respect to hurricanes,” and although rates are coming in, they continue to see rate adequacy and strong opportunities to deploy additional capital at high ROE. In other words: the stronger balance sheet from avoided catastrophe events and growth opportunities are more than offsetting the lower rates. As they stated on the call: “rates went up 50% in 2023, and over the last two quarters we’re talking about rate changes in the 10-ish percent range.” JPM estimated a 4-8% profit lift for reinsurers on the quarter given this dynamic, and the reinsurance subsector outperformed primary carriers in Q3.

By and large, insurtechs once again continued to outperform. Lemonade (LMND, +22%) traded way up on both its August and November quarter results. Q2 results showed 29% y/y growth of in-force premium, the 7th consecutive quarter of acceleration (bested in November by an 8th sequential increase that came in at 30%). Q2 revenue was up 35% y/y, outpacing premium growth, and reflecting big improvements in both gross loss ratio and cross-sell conversion in the previously challenged auto segment. With growth continuing to ramp and gross losses falling, the stock is up >360% in 24 months. ROOT, which started its recovery earlier and is further along in its cycle, had more paltry PIF growth of 12% and traded lower on its report, but remains up >135% over 12 months. In a quarter marked by P&C underperformance, the insurtech segment remains a bright spot.

Trends in rates, competition, natural catastrophes, and overall macro will continue to drive performance of the P&C sector over the remainder of the year. We continue to believe that a focus on underserved segments and differentiated profitability offers long term opportunities for P&C carriers and distributors that will persist regardless of near-term trends in pricing. If, like us, you’re watching this space closely or building something new, we’d love to hear from you — feel free to reach out to me at adam@equal.vc.